AMLA 2026 will not make every EU bank reject non-resident clients overnight. It will do something quieter and more practical: force banks to explain, compare and defend their AML risk scoring before the EU Anti-Money Laundering Authority begins direct supervision in 2028. For foreign clients, that means the old question, “Can I open an account?”, becomes a sharper one: “Can my source of wealth, tax residence, ownership chain and payment story survive a second review?”

That is the part most regulatory summaries miss. AMLA is not just a Brussels acronym. For a non-resident client, AMLA 2026 is the year when vague comfort stops working. A bank may still like your assets, your passport and your fee potential. However, if the file reads messy, the relationship manager loses the argument before the account committee even starts.

The uncomfortable truth is that many clean clients will look risky because their story arrives in the wrong order. A founder sells a company, moves residence twice, holds funds through a family vehicle, pays from a crypto exchange or a UAE free zone entity, and then wonders why a European bank hesitates. None of those facts is automatically fatal. Together, though, they create work. Banks dislike work when the margin is not obvious.

AMLA 2026 is not a new form. It is a new scoring language.

Here is the banker’s version. AMLA 2026 asks a simple question: can the bank explain this client without guesswork? If the answer is yes, the account has a chance. If the answer is no, the file drifts toward delay, extra checks or refusal.

The EU created AMLA through Regulation (EU) 2024/1620, and the agency is moving from institution-building into practical supervisory preparation. The point is not to replace every national supervisor at once. The point is to make the riskiest parts of the EU financial system speak a common AML language, especially when clients, money and ownership structures cross borders.

AMLA will directly supervise selected high-risk banks and other financial firms from 2028. Before that, AMLA 2026 matters because banks will prepare for selection, peer comparison and new EU-level review long before the first formal inspection lands. Actually, scratch that: the best banks have already started. The slower ones will catch up when their board asks why the client risk book looks harder to defend than a competitor’s.

For foreign clients, the change is subtle but sharp. In the old model, a bank could accept a client if its internal policy, national regulator and risk appetite lined up. In the AMLA-era model, the bank must also imagine how the file looks under a more common EU standard. That second audience changes behavior. It pushes banks toward fewer exceptions, better proof and cleaner reasons for accepting cross-border risk.

The timeline shows 2024 adoption of the EU AML package, 2026 AMLA supervisory preparation, 2027 single-rulebook application and 2028 direct supervision of selected high-risk financial institutions.

Why non-resident clients will feel AMLA 2026 first

Foreign clients sit where banks already feel exposed: cross-border tax home, foreign source of wealth, unfamiliar papers, multi-country payments, and sometimes a mismatch between where wealth was made and where wealth is now held. AMLA 2026 does not invent those concerns. It makes them harder to wave away.

A resident salaried client with local tax filings is easy to understand. A foreign founder with a holding company, an old operating business, a recent exit, a new tax home and three correspondent-bank payment routes is not. The bank must connect identity, control, wealth creation, tax logic and payment behavior. If one link is weak, the risk score rises.

This is why a bank account rejected for AML risk often feels unfair. The client hears “high risk” as an accusation. The bank means something colder: the file takes too much explanation for the expected revenue. That distinction matters. A client can fix explanation. A client cannot argue a committee into liking uncertainty.

Easy Global Banking already sees this pattern across Swiss and Singapore account work: the paper set may be technically complete, yet the file still fails because the papers do not tell one clean story. For a deeper companion piece, read The AML Risk Score Explained and Why Was My Swiss Bank Account Application Rejected?.

The six risk signals EU banks will re-score before 2028

AMLA direct supervision will not turn banks into identical machines. Still, the direction is clear: EU banks will need a cleaner way to show why Client A is acceptable, why Client B needs enhanced due diligence, and why Client C should be declined. The six signals below are where non-resident clients usually gain or lose the room.

The risk map ranks source of wealth, geography, ownership chain, tax residence, payment route and product fit by likely review pressure for non-resident clients in an AMLA 2026 banking file.

First, source of wealth becomes the center of gravity. Not source of funds alone. Source of funds explains the immediate transfer. Source of wealth explains how the client became wealthy in the first place. A sale agreement, audited company accounts, tax records, dividend history and bank statements should line up. If they do not, the file starts to look like a collage.

Second, geography matters even when the client personally looks clean. FATF monitoring, EU high-risk third-country exposure, sanctions proximity, politically exposed person links, and corruption perception all shape the bank’s appetite. Quick caveat before we keep going: nationality alone should not decide the outcome. In practice, though, geography tells the compliance team where to look harder.

Third, control complexity needs a reason. A foundation, trust, holding company or free zone vehicle can be perfectly legitimate. However, the bank will ask why that structure exists, who controls it, who benefits from it, how it is taxed, and why the account belongs in the EU rather than where the business actually operates. Structure without purpose looks evasive, even when it is legal.

Fourth, the tax home must match the banking story. If the client claims residence in Country A, receives business income from Country B, holds a company in Country C and wants portfolio management in Country D, the file needs a clear CRS story. The bank does not want to discover later that the tax explanation was an afterthought. For the tax side of bank paperwork, see CRS Tax Residency Privacy.

Fifth, payment behavior will carry more weight. A client who opens a private banking relationship and immediately sends funds to unrelated third parties has created a different file from a client funding a custody portfolio from a known exit account. Payment purpose, counterparty logic and corridor risk matter. This is where the SWIFT Payment Rejected by an Intermediary Bank problem starts before the wire is even sent.

Sixth, product fit becomes a quiet gatekeeper. A bank may tolerate more review work for a serious private banking mandate than for a low-balance transactional account. That sounds harsh because it is. Still, it explains many rejections that clients read as moral judgments. The bank is often making an operational decision: too much risk work, too little expected relationship depth.

What changes before AMLA direct supervision starts in 2028

The mistake is waiting for 2028. Banks do not prepare for new supervision by changing files on the morning the supervisor arrives. They review portfolios early, clean risk-rating logic, close weak relationships, refresh stale KYC files and reduce exceptions that would be embarrassing to defend later.

That means AMLA 2026 will show up in three places. New account openings will get more structured. Existing clients will face sharper periodic reviews. Borderline cases will move faster toward “no” because the cost of keeping them rises. None of this requires a dramatic press release. It happens inside onboarding memos, risk committees and remediation projects.

There is a practical reason for the early shift. The EU’s new AML Regulation, Regulation (EU) 2024/1624, creates rules that apply across the bloc. Once that rulebook is in force, banks cannot rely as comfortably on local habits. They need files that survive comparison. The file does not need to be perfect. It does need to make sense.

The AMLA timeline shows the 2024 EU AML package, AMLA becoming operational in 2025, bank alignment in 2026, single-rulebook application in 2027 and direct supervision starting in 2028.

The AMLA 2026 document file that gives a non-resident client a chance

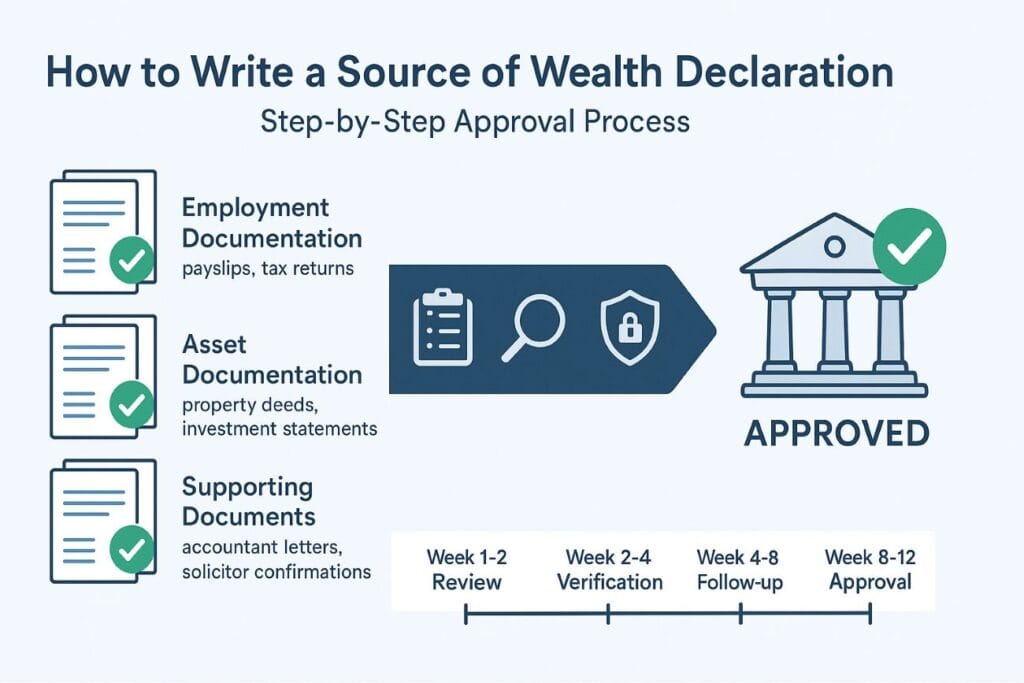

The winning AMLA 2026 file is not the thickest file. It is the file that a risk committee can explain in two minutes without improvising. That is the standard clients should use. If your own advisor cannot summarize the wealth story, tax home, control structure and account purpose without flipping through 80 pages, the bank probably cannot either.

Start with identity and residence. Passport, residence permit, proof of address and tax identification numbers should agree with the application narrative. If the client recently moved, say when and why. Do not let the bank discover the move from a utility bill, a CRS form and a payment reference that all point in different directions.

Then build the source-of-wealth chain. For an entrepreneur, that might mean incorporation records, audited accounts, sale and purchase agreement, closing statement, tax filing and the bank statement where the proceeds landed. For inherited assets, it might mean probate documents, estate distribution records and historic account statements. For investment wealth, it might mean broker statements, tax records and a portfolio history. Boring is good here. Boring proves continuity.

Next, explain control. If a company, foundation, trust or partnership sits between the person and the money, the bank needs true-owner data, control rights, protector or director roles, and the reason the structure exists. A pretty chart helps, but only if the chart matches legal papers. Many files fail because the chart says one thing and the registry extract says another. Small mismatch, big headache.

Finally, show account purpose. “Wealth management” is too vague. A stronger purpose sounds like this: “The client wants to custody post-exit liquid assets, invest through a discretionary mandate, receive dividend distributions twice a year and make limited family expenses from the account.” That tells the bank what activity to expect. It also gives the monitoring team a baseline for unusual transactions.

| Risk question | Documents that answer it | Common failure |

|---|---|---|

| Who is the client? | Passport, proof of address, tax IDs, residence evidence | Residence story differs across forms |

| Who controls the assets? | UBO chart, registers, trust or foundation documents, board minutes | Control rights hidden behind titles |

| How was wealth created? | Sale agreement, accounts, tax filings, inheritance records, broker history | Only immediate source of funds is shown |

| Why this bank? | Mandate description, custody need, jurisdiction logic, expected activity | Account purpose sounds generic |

| What will move through the account? | Expected inflows, counterparties, payment corridors, investment plan | Payments contradict stated purpose |

This is also where crypto-linked clients need discipline. A bank may accept crypto wealth if the fiat story is complete: wallet history, exchange records, tax treatment, realized gains, clean fiat conversion and a credible explanation of how the assets were acquired. If crypto proceeds enter a bank file as a screenshot and a shrug, expect enhanced due diligence. For that specific problem, use How to Document Crypto Income for a Bank Application.

Who should act before the bank asks

AMLA 2026 matters most for clients whose banking profile depends on cross-border judgment. That includes non-resident HNWIs, founders after an exit, clients from FATF-monitored countries, politically exposed persons and close associates, crypto-liquidity clients, free zone company owners, global families with trusts or foundations, and anyone using a European bank mainly as a neutral custody base.

If that sounds broad, it is. Still, the practical priority is narrower. Act first if your account was opened years ago under a softer review standard, if your tax home changed, if your company was sold, if your asset mix now includes digital assets, if a family structure was added, or if your payments no longer match the original account purpose.

Existing clients often underestimate this. They assume the hard part was opening the account. In the AMLA 2026 cycle, the harder part may be keeping the file credible after the facts changed. A bank can accept you in 2022 and still question you in 2026 because the risk story moved while the KYC file stayed frozen.

New clients should treat the application like a banker’s memo, not a document dump. That means a one-page case story, a clean UBO chart, a source-of-wealth timeline, a tax-home note and an expected-use note. The papers support the story. They do not replace it.

How to lower AML risk without pretending risk does not exist

The worst AMLA 2026 strategy is trying to look simple when the facts are complex. Banks notice. A better strategy is to make complexity legible. If there are three jurisdictions, say why. If a holding company exists, explain its tax, succession or asset-protection purpose. If a payment corridor looks unusual, connect it to a contract, sale, dividend or investment plan.

Do not hide adverse facts. A historic investigation, a difficult jurisdiction, a failed previous application or a crypto sale is easier to manage when the bank hears it from you with evidence. When the bank finds it later, the same fact feels different. Not necessarily worse in law, but worse in trust. That is usually enough.

Also, do not over-lawyer the file. Some clients send a legal opinion when the bank needs a bank statement. Others send a trust deed when the bank needs to know who can remove the trustee. The file should answer the reviewer’s question at the level the reviewer needs. Anything more creates fog.

A practical sequence works best. First, map the client: identity, tax home, tax position and roles. Second, map the wealth: origin, growth, sale or transfer and current location. Third, map control: legal owner, true owner, decision maker and economic beneficiary. Fourth, map activity: expected inflows, outflows, investment use and countries involved. If a bank can follow those four maps, the risk score may still be elevated, but the rejection risk falls.

The checklist describes four file maps: client, wealth, control and activity. Each map helps a bank understand and defend a non-resident client’s AML risk under AMLA 2026.

The strategic point: AMLA 2026 rewards clients who are easy to defend

AMLA 2026 is not the end of non-resident banking in Europe. It is the end of lazy non-resident files. That difference is everything. Strong clients will still get banked. Weakly explained clients will be pushed toward delay, remediation, limited product access or rejection.

So the right question is not, “Will AMLA make me high risk?” The better question is, “Can my bank defend my risk rating after a reviewer reads the file cold?” If the answer is no, fix the file before the review cycle fixes it for you. And by “fix,” I do not mean polish the cover letter. I mean make the facts line up.

For clients already facing friction, the next move is a pre-application or pre-review diagnostic: identify the weak link, rebuild the source-of-wealth narrative, align tax residence with CRS forms, clarify ownership control and remove payment ambiguity. A good bank file does not ask compliance to trust you. It gives compliance less to doubt.

That is the real AMLA 2026 lesson. The safest client is not always the richest client, or the client with the most documents. It is the client whose story survives being retold by someone else in a risk meeting.

FAQ: AMLA 2026 and non-resident bank account risk

Will AMLA 2026 make EU banks reject all non-resident clients?

When does AMLA direct supervision start?

What is the biggest AMLA 2026 risk for a foreign client?

Can a client lower an AML risk score?

References

EU Anti-Money Laundering Authority: official AMLA website (opens in new tab)

Regulation (EU) 2024/1620 establishing AMLA (opens in new tab)

Regulation (EU) 2024/1624 on AML/CFT requirements (opens in new tab)

European Commission: AML/CFT at EU level (opens in new tab)

FATF: jurisdictions under increased monitoring and high-risk jurisdictions (opens in new tab)