Your AML risk score is a number — or a tier label like “low,” “medium,” or “high” — that your bank assigns to you the moment you open an account. Once you understand how AML risk score banking works, the entire compliance process starts to make sense. This Customer Risk Rating (CRR) determines everything: how fast your application is approved, how much paperwork you’ll face, whether your wire transfers sail through or get frozen for weeks, and ultimately, whether the bank even wants you as a client. Yet most people never see their score and have no idea what drives it.

Here’s the uncomfortable truth. Banks don’t reject clients because they’re criminals. They reject clients because the compliance file is messy. A confusing source-of-wealth narrative, an outdated corporate structure diagram, a passport from a jurisdiction on the FATF monitoring list — these red flags inflate your AML risk score before a human compliance officer even reads your name. And once your score crosses a threshold, Enhanced Due Diligence kicks in, dragging the process out for months.

What most people miss is that this score isn’t fixed. It’s dynamic. You can actively shape it — and the clients who walk into a bank with a pre-structured compliance dossier consistently land in lower risk tiers than those who wing it. This article is the AML risk score banking explained from your side of the desk, not the compliance officer’s. We break down exactly how risk scoring works, what each tier means in practice, and seven concrete steps to improve your AML profile before you ever submit an application.

How Banks Actually Calculate Your AML Risk Score

Every bank builds its own risk scoring model, but the architecture follows a pattern mandated by FATF’s risk-based approach (RBA). The Wolfsberg Group — a consortium of 13 global banks including UBS, Credit Suisse, and HSBC — publishes guidelines that most private banks quietly adopt. In practice, the process looks like this:

The critical detail: steps 1 and 2 happen before a relationship manager reads your file. Automated screening tools make the first impression on your AML risk score. If your profile triggers multiple flags — say, a construction business owner with a Turkish passport sending funds from a UAE entity — the risk scoring model assigns a preliminary “high risk” label that colors every human review afterward. What separates successful applicants from rejected ones often comes down to how their information is pre-structured and presented. Our team at Easy Global Banking builds these compliance dossiers professionally — learn more about how we prepare clients for Swiss bank account opening (opens in new tab).

Those numbers explain why banks are paranoid. With $2 trillion in laundered money swirling through the system and only 1% getting caught, regulators have made it personally costly for compliance officers to miss red flags. In 2024, TD Bank paid a record $1.3 billion fine for BSA violations. Every compliance officer remembers that number when reviewing your file.

The 5 Core Risk Factors That Shape Your AML Risk Score in Banking

Not all risk factors carry equal weight. A McKinsey analysis of AML risk-rating models found that most banks overweight some factors and ignore others — often producing scores that misclassify thousands of legitimate clients as high risk. Here’s what actually moves the needle on your Customer Risk Rating.

1. Geographic Risk — The Silent Score Inflator

Geography alone can account for 30% of your total AML risk score. Your passport country, tax residency, and the jurisdictions where your businesses operate all feed into the customer risk rating. A German entrepreneur running a software company scores differently than a Brazilian entrepreneur running the exact same business — and neither one chose their passport.

FATF maintains a “grey list” — formally called jurisdictions under increased monitoring — that included 23 countries as of early 2026. Holding citizenship in or receiving funds from these jurisdictions automatically bumps your risk tier. But even non-listed countries carry varying weights. Swiss banks, for example, internally classify Middle Eastern and Central Asian jurisdictions at medium risk even when they’re not on the FATF list.

What you can control: disclose every current citizenship and let the bank specify the primary identity document. Do not lead with a supposedly lower-risk passport to conceal another nationality. Our second-passport bank compliance guide explains how banks reconcile citizenship, residence, tax residence and wealth origin. If funds transit through a higher-risk jurisdiction, prepare a documented commercial explanation and complete transaction trail.

2. Source of Wealth and Source of Funds

This is where most applications fail — and where your AML risk score can spike overnight. Banks distinguish between two concepts that clients constantly confuse. Source of Wealth (SoW) means the historical origin of your entire net worth — how you built your fortune over a lifetime. Source of Funds (SoF) is narrower: where the specific money entering this account came from. A tech founder who sold a company for $20 million has a clear SoW. But if the sale proceeds sat in a Cayman Islands trust for three years before arriving at a Swiss bank, the SoF narrative gets complicated — and the client due diligence score rises sharply.

In practice, compliance officers want a narrative that traces money from origin to deposit in a logical, documented chain. Gaps in this chain are the single fastest way to get flagged for Enhanced Due Diligence.

3. Customer Type and PEP Status

Politically Exposed Persons (PEPs) automatically receive higher risk scores. The definition is broader than most people realize — it extends to family members and close associates of government officials, not just the officials themselves. If your brother-in-law was a deputy minister eight years ago, some banks still classify you as a PEP associate.

Corporate structures add complexity. A single individual with one passport is simple. A person who controls three offshore entities through a family trust, with nominee directors in two jurisdictions? That profile screams complexity to a compliance algorithm. The Wolfsberg Group’s guidance is clear: complexity itself is a risk factor, even when the structure is perfectly legal.

4. Product and Channel Risk

Not all banking products carry the same risk weight. Private banking relationships attract more scrutiny than standard retail accounts — which is precisely why understanding the difference between Swiss private and retail banking (opens in new tab) matters before you apply. Correspondent banking, trade finance, and cryptocurrency custody all carry elevated risk weights.

The delivery channel matters too. Remote account opening — especially when the client never visits the bank in person — increases the risk score versus in-branch verification. Video identification helps but doesn’t fully offset this factor.

5. Transaction Behavior

This factor only becomes relevant after you’ve opened the account, but it continuously recalibrates your score. Banks set expected activity profiles during onboarding: anticipated transaction volumes, typical counterparties, expected geographies. When your actual behavior deviates significantly from these expectations — a sudden $500,000 wire to a country you’ve never mentioned, for instance — the monitoring system flags it.

Dynamic risk scoring, which AMLYZE and other compliance platforms now promote, means your AML risk score changes monthly based on actual behavior. Consistent, predictable transaction patterns that match your stated profile will gradually lower your customer risk rating over time. This is one way to genuinely improve your AML profile at the bank without submitting a single new document.

Low, Medium, and High Risk: What Each AML Risk Score Tier Actually Means for You

Banks won’t show you a dashboard with your risk score. But your experience reveals which tier you occupy. Here’s what each level triggers in practice — from the client’s perspective:

| Factor | Low Risk | Medium Risk | High Risk |

|---|---|---|---|

| Due Diligence Level | Standard CDD — basic identity + address verification | Standard CDD plus additional SoW/SoF documentation | Enhanced Due Diligence (EDD) — deep-dive investigation |

| Onboarding Time | 1–3 weeks | 3–6 weeks | 2–6 months (if accepted at all) |

| Periodic Review | Every 3–5 years | Every 1–2 years | Every 6–12 months |

| Transaction Monitoring | Standard automated alerts | Lower alert thresholds; some manual review | Aggressive thresholds; frequent manual review |

| Wire Transfer Experience | Same-day or next-day processing | Occasional holds for large or unusual transfers | Multi-day holds common; compliance calls likely |

| Relationship Manager Access | Self-service or junior RM | Dedicated RM with periodic check-ins | Senior RM + compliance officer oversight |

| Risk of Account Closure | Very low | Low to moderate (if profile deteriorates) | Elevated — bank may exit the relationship |

From the field: Most private banking clients in Switzerland and Singapore fall into the medium risk tier. That’s normal. It doesn’t mean you’re suspected of anything — it simply means you have international elements in your profile that require additional documentation. The goal isn’t to be “low risk” at all costs. It’s to be medium risk with a clean, well-documented file. That’s the sweet spot for acceptance.

This scoring process is becoming more structured across Europe. Our analysis of AMLA 2026 and EU bank risk scoring explains why cross-border clients should expect more consistent data fields before direct supervision starts in 2028.

CDD vs. EDD: The Client Due Diligence Experience You’ll Actually Face

Every banking client goes through Customer Due Diligence (CDD). FATF Recommendation 10 mandates it globally — there’s no opting out. The question is which level of CDD you’ll face, because the jump from standard to enhanced changes your onboarding experience dramatically.

Standard CDD is straightforward. You provide your passport, a recent utility bill, a brief explanation of what you do for a living and where your money comes from. Most EU or North American salaried professionals clear standard CDD in under two weeks.

Enhanced Due Diligence, though, is a different animal. EDD applies when any risk factor pushes your CRR above the bank’s internal threshold. In practice, EDD means the bank will request certified copies of corporate registrations going back years, audited financial statements, detailed wire transfer histories, references from other banks, and sometimes even a face-to-face interview with the compliance department. For clients opening accounts in Singapore — where MAS requirements are among Asia’s strictest — our team pre-builds the EDD-ready dossier before the bank asks (opens in new tab).

The FATF’s 2025 guidance update actually tried to soften this. It encouraged banks to apply Simplified Due Diligence (SDD) for genuinely low-risk clients — acknowledging that overly cautious approaches had been excluding legitimate customers from the financial system. Approximately 1.4 billion people worldwide remain unbanked, and FATF recognized that excessive compliance requirements were part of the problem. But the reality on the ground is that most banks still default to caution, especially for non-resident, non-EU clients.

What Banks See When They Screen Your Name

Before a compliance officer reads a single document, your name has already been processed through screening databases. The two dominant ones are LSEG’s World-Check (formerly Refinitiv World-Check) and Dow Jones Risk & Compliance. Here’s what a typical screening produces:

The false positive problem is massive. If your name resembles someone on a sanctions list, the system flags you. A “Mohamed Ali” in Zurich will consistently trigger hits that have nothing to do with him. These false positives don’t automatically make you high risk, but they create friction — someone has to manually investigate and clear them. Banks running 250 to 2,000 screening alerts per day (depending on the institution) often lack the bandwidth for quick resolution.

Adverse media screening deserves special attention. Banks now use natural language processing to scan global news in real time. An old lawsuit, a political dispute, even being mentioned alongside someone under investigation — these generate “adverse media” hits. The hits may be irrelevant to money laundering, but they add points to your risk profile.

What you can do: Google yourself. Search your name alongside your company names. If old, misleading, or contextually damaging results appear, prepare written explanations before you apply. A proactive approach — what compliance consultants call a “pre-emptive narrative” — dramatically reduces processing time and keeps your AML risk score from spiking on a screening hit that has nothing to do with financial crime.

Which Jurisdictions Inflate Your AML Risk Score the Most?

Not all country risks are equal. Here’s a practical breakdown of how different passport and residency jurisdictions typically affect your risk scoring in Swiss and Singaporean private banking. These are illustrative ranges based on common bank models — actual weights vary by institution.

A crucial nuance: it’s not just your passport that matters. Where your funds originate can carry even more weight in the AML risk score calculation. A Swiss citizen receiving regular wire transfers from a company registered in a FATF grey-listed jurisdiction will score higher than expected for their nationality alone. The EGB AML Risk Calculator — a tool we developed for our pre-assessment consultations — weighs all these factors together before we even approach a bank.

7 Proven Steps to Improve Your AML Risk Score Before Applying

This is the part nobody else writes about, because the compliance industry addresses banks, not clients. But as someone who helps HNWIs open non-resident bank accounts across multiple jurisdictions (opens in new tab), I can tell you: the difference between acceptance and rejection is almost always preparation, not profile.

Step 1: Audit Your Digital Footprint

Run your full name through Google, World-Check (if you have access through a compliance consultant), and adverse media databases. Search your company names too. Banks will find whatever you find — and more. Identify anything that needs context or explanation, and write a one-page narrative addressing each item before the bank raises it.

Step 2: Simplify Your Corporate Structure

Every layer of ownership between you and your funds adds risk points. If you control a BVI company that owns a UAE entity that holds a Singapore subsidiary — and the bank account is for the Singapore entity — compliance officers will need to trace beneficial ownership through each layer. Where possible, flatten structures before applying. If the complexity is legally necessary (and it often is), document every layer with current registry extracts, shareholder agreements, and a visual org chart.

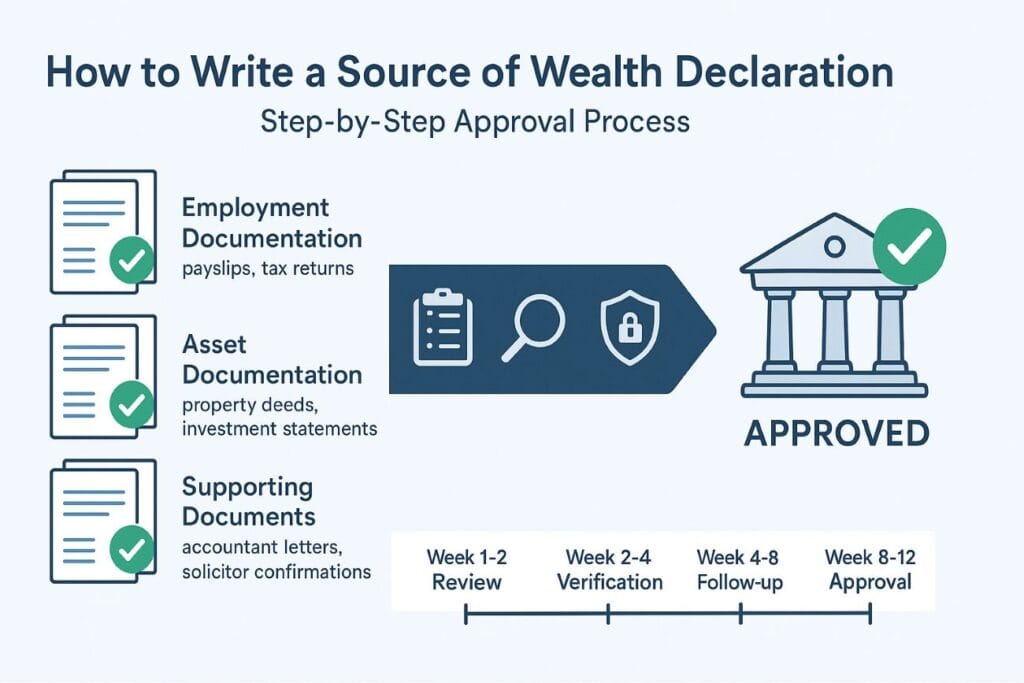

Step 3: Build a Source of Wealth Timeline

Don’t just state “entrepreneur” as your occupation. Build a chronological narrative: founded Company X in 2009, grew revenue to $Y by 2015, sold 60% stake to private equity fund Z in 2018 for $W, invested proceeds in real estate and public equities. Include supporting documents at each milestone — contracts, tax returns, audited financials. This is what compliance consultants call a “SoW dossier,” and it should tell a story that a compliance officer can verify in hours, not weeks.

Step 4: Consolidate Your Funds Before Transfer

Money arriving from five different accounts in three countries triggers more flags than a single, well-documented transfer from one account. Before you open a new banking relationship, consolidate your funds in one existing account. Keep a paper trail showing the consolidation. When you eventually wire the initial deposit, the receiving bank sees one clean transfer from one institution — not a fragmented puzzle.

Step 5: Prepare Your Tax Compliance Documentation

Since the Automatic Exchange of Information (AEOI) went into effect, Swiss banks report your account to your home country’s tax authority annually. Banks know this. If your tax affairs are messy, they assume the relationship will eventually create problems. Come armed with your latest tax return, proof of tax residency (a certificate from your local authority), and — if applicable — documentation showing you’ve declared any existing foreign accounts.

Step 6: Request a Reference Letter from Your Current Bank

A compliance reference letter from a reputable existing bank is the single most underrated tool for lowering your AML risk score at a new institution. It signals that another regulated institution has already done the due diligence and accepted you. Request it specifically: ask your current bank to confirm account tenure, transaction history consistency, and the absence of compliance issues. Not all banks provide these willingly, so allow 2–4 weeks.

Step 7: Use a Regulated Intermediary for Introduction

Applying cold — walking into a bank without an introduction — almost guarantees a higher initial risk score. Compliance algorithms treat unsolicited applications from non-residents as inherently riskier. A regulated financial intermediary, like a licensed external asset manager or a FINMA-supervised consultant, can introduce your pre-vetted dossier directly to a senior relationship manager. The bank treats introduced clients differently because the intermediary’s own reputation (and regulatory standing) is on the line.

The SAR Trigger: What Happens When Your Bank Files a Suspicious Activity Report

A Suspicious Activity Report (SAR) is the nuclear option in AML compliance. When a bank files a SAR with its national Financial Intelligence Unit (FIU), you won’t know about it — “tipping off” the client is illegal in most jurisdictions. But the consequences are real. SARs can trigger law enforcement investigations, asset freezes, and in many cases, the bank will proactively close your account to limit its own regulatory exposure.

SARs aren’t only filed when a bank suspects actual money laundering. They’re also filed defensively — when a compliance officer can’t satisfactorily explain unusual activity and doesn’t want to risk personal liability for not reporting it. This defensive filing culture means that confusing but innocent behavior (a sudden large deposit you didn’t pre-notify, funds from a new country you didn’t mention during onboarding) can trigger a SAR and permanently damage your AML risk score across the banking system.

Prevention matters far more than response. Once a SAR is filed, your options shrink dramatically. Before that point, clear communication with your relationship manager about any expected changes in activity patterns — a property sale, an inheritance, a new business venture — prevents the compliance team from being surprised.

Practical tip: Whenever you expect a transaction that deviates from your usual profile — whether in amount, geography, or counterparty — email your relationship manager before the funds move. A one-paragraph heads-up with supporting documentation (“I’m receiving $300K from the sale of my apartment in Lisbon; here’s the notarized sales contract”) costs you two minutes and saves you months of potential investigation.

Readers who want the short history of the tool can also see why EGB launched its free AML risk calculator and what the first version was designed to test.

How the EGB AML Risk Calculator Works: Self-Assess Before You Apply

At Easy Global Banking, we developed an internal AML risk scoring model specifically for pre-assessing clients before we approach any bank. It’s not the bank’s risk scoring model — no external party can replicate a bank’s proprietary compliance algorithm — but it’s built on the same risk-based approach KYC principles and weighted against real-world acceptance data from Swiss and Singaporean institutions.

During a private consultation, we evaluate your profile across the same five factors described above: geographic risk, source of wealth/funds clarity, customer type and PEP proximity, product complexity, and expected transaction patterns. Each factor receives a weighted score. The output tells us which banks are likely to accept your profile, which will require EDD, and which we shouldn’t approach at all — saving you from rejections that leave marks on your compliance record.

This pre-assessment also reveals fixable gaps. Maybe your corporate structure needs one less layer. Maybe your SoW narrative needs a third-party valuation to be convincing. Maybe we need to address an adverse media hit proactively. These are problems we solve before the bank ever sees your name.

A critical distinction: professional compliance preparation does not lower your AML risk score. A PEP associate is always classified as high risk — that classification is regulatory, not negotiable. What changes is whether the bank accepts the file despite the high-risk tier. A Central Asian PEP associate applying cold has roughly a 10% chance of acceptance at a Swiss private bank. That same individual, presented through a regulated intermediary with a fully documented SoW narrative, a pre-cleared World-Check explanation, and a simplified corporate structure, sees acceptance probability rise to approximately 45%. The risk score stays high. The EDD process still applies. But the bank gains the confidence to say yes instead of defaulting to rejection.

Frequently Asked Questions About AML Risk Scores

Can I request my own AML risk score from my bank?

No. Banks treat Customer Risk Ratings as confidential internal documents. Sharing your score could constitute “tipping off” in jurisdictions where that’s regulated, and it would reveal the bank’s proprietary risk model. However, you can infer your tier from observable signals: how long onboarding takes, whether you’re asked for Enhanced Due Diligence documentation, and how frequently the bank requests profile updates.

Does a high AML risk score mean I’m suspected of money laundering?

Not at all. A high risk score means your profile carries characteristics that statistically correlate with higher money laundering probability — like operating in certain jurisdictions or industries. Perfectly legitimate clients regularly receive high risk ratings. The rating determines the level of scrutiny applied, not suspicion of wrongdoing.

How often does my AML risk score change?

Traditional banks re-score during periodic reviews — every 1 to 5 years, depending on your tier. But modern dynamic risk scoring systems update continuously based on your transaction behavior, screening hits, and external data changes (such as your country being added to or removed from the FATF grey list). Some banks now adjust scores daily using AI-driven monitoring platforms.

What is the difference between a risk score and a risk rating?

The risk score is the numerical output — for example, 42 out of 100. The risk rating is the tier label that score maps to — low, medium, or high. Banks use different scales; some use 0–100, others 1–5, and some assign points per factor that aggregate to a total. The rating tiers determine which due diligence procedures apply. Both terms are used interchangeably in the industry, which causes confusion.

Can a rejected bank application affect future AML risk scores at other banks?

Banks don’t share rejection data in a centralized database the way credit bureaus do. However, if a rejection triggers a SAR filing, that report enters the FIU’s system and may be visible during screening at future banks. Additionally, some compliance databases track “declined relationships” as adverse information. The safest approach is to avoid applying to banks where rejection is likely — which is exactly what a pre-assessment with a regulated intermediary prevents.

Does cryptocurrency wealth automatically trigger a high-risk AML score?

In most Swiss and Singaporean private banks, yes — cryptocurrency-derived wealth pushes the product risk factor significantly higher. Some banks won’t accept crypto wealth at all, while others specialize in it. The key to acceptance is providing a verifiable on-chain transaction history and, ideally, a compliance report from a blockchain analytics firm like Chainalysis or Elliptic that traces your funds from mining or exchange purchase to current holdings.

Understanding your AML risk score in banking isn’t about gaming the system. Banks need these controls — the $2 trillion money laundering problem is real, and the 1% detection rate proves the system needs to work harder, not softer. But there’s a difference between being high risk because your file is poorly prepared and being high risk because your profile genuinely warrants scrutiny. Most international clients fall into the first category, and that’s entirely fixable with the right banking strategy and institutional selection (opens in new tab).

The risk-based approach that FATF mandates is supposed to be proportionate. Simplified due diligence for low-risk bank clients, enhanced scrutiny for genuinely complex profiles, and a thoughtful middle ground for everyone else. When you present a professionally structured compliance dossier — with a clean SoW narrative, simplified structures, proactive adverse media responses, and a credible intermediary introduction — you make it easy for the bank to assign the AML risk score you deserve: one that gets approved.

References

- FATF Recommendations — International Standards on Combating Money Laundering (Updated October 2025) (opens in new tab)

- McKinsey — Flushing Out the Money Launderers with Better Customer Risk-Rating Models (opens in new tab)

- FFIEC BSA/AML Examination Manual — BSA/AML Risk Assessment (opens in new tab)

- EY Switzerland — How to Successfully Operationalize Your Client Risk Rating Model (opens in new tab)

- FATF — Guidance on Financial Inclusion and AML/CFT Measures (2025) (opens in new tab)