Open a Singapore Bank Account as a Non-Resident

A private banking and wealth account opening service for internationally mobile clients, founders, family offices, and offshore structures. We prepare your Singapore KYC file, confirm accredited-investor readiness, match the right banking route, and coordinate banker-led onboarding.

Singapore private banking

For non-resident HNWIs, founders, family offices, and corporate structures.

USD 3m+ target route

Our core Singapore route is designed for meaningful private banking balances, not low-balance retail accounts.

Accredited investor ready

We help position your file around Singapore AI classification, source-of-wealth evidence, and bank appetite.

Banker-led onboarding

Remote coordination is possible, but approval remains compliance-led and relationship-led.

Singapore Banking for Non-Residents Is a Qualification Problem

Most applicants ask, “Can I open a Singapore bank account remotely?†The better question is whether your profile is attractive enough for the right Singapore banking desk. For non-residents, the account decision turns on investable assets, source of wealth, tax residence, nationality, account purpose, and whether the relationship creates enough value for the bank to absorb the compliance work.

Easy Global Banking turns that problem into a structured application. We pre-screen your risk profile, build the source-of-wealth narrative, align your documents with Singapore KYC expectations, and introduce the case to a suitable private banking or wealth route.

Best fit: non-resident clients with clean source-of-wealth evidence, international banking needs, and a realistic private banking balance. This page is not for low-balance retail apps, student accounts, or simple local salary accounts.

Singapore Private Banking Minimums for Non-Residents

Singapore does not have one official private banking minimum. Each bank applies its own commercial threshold and risk appetite. As a working rule, USD 3m+ in investable assets is the realistic route for our Singapore private banking service. Lower balances can be reviewed only where the profile is exceptionally clean and the banking purpose is strong.

| Investable assets | Likely Singapore route | What the bank will test |

|---|---|---|

| USD 1m-3m | Selective review only | Clean nationality/residence, simple wealth story, and strong reason for Singapore. |

| USD 3m-5m | Core private banking route | Accredited investor readiness, source of wealth, tax residence, expected account activity. |

| USD 5m-10m | Priority relationship route | Investment mandate, custody needs, multi-currency liquidity, structure transparency. |

| USD 10m+ | Family office / complex wealth route | Entity ownership, beneficiaries, cross-border tax position, enhanced due diligence. |

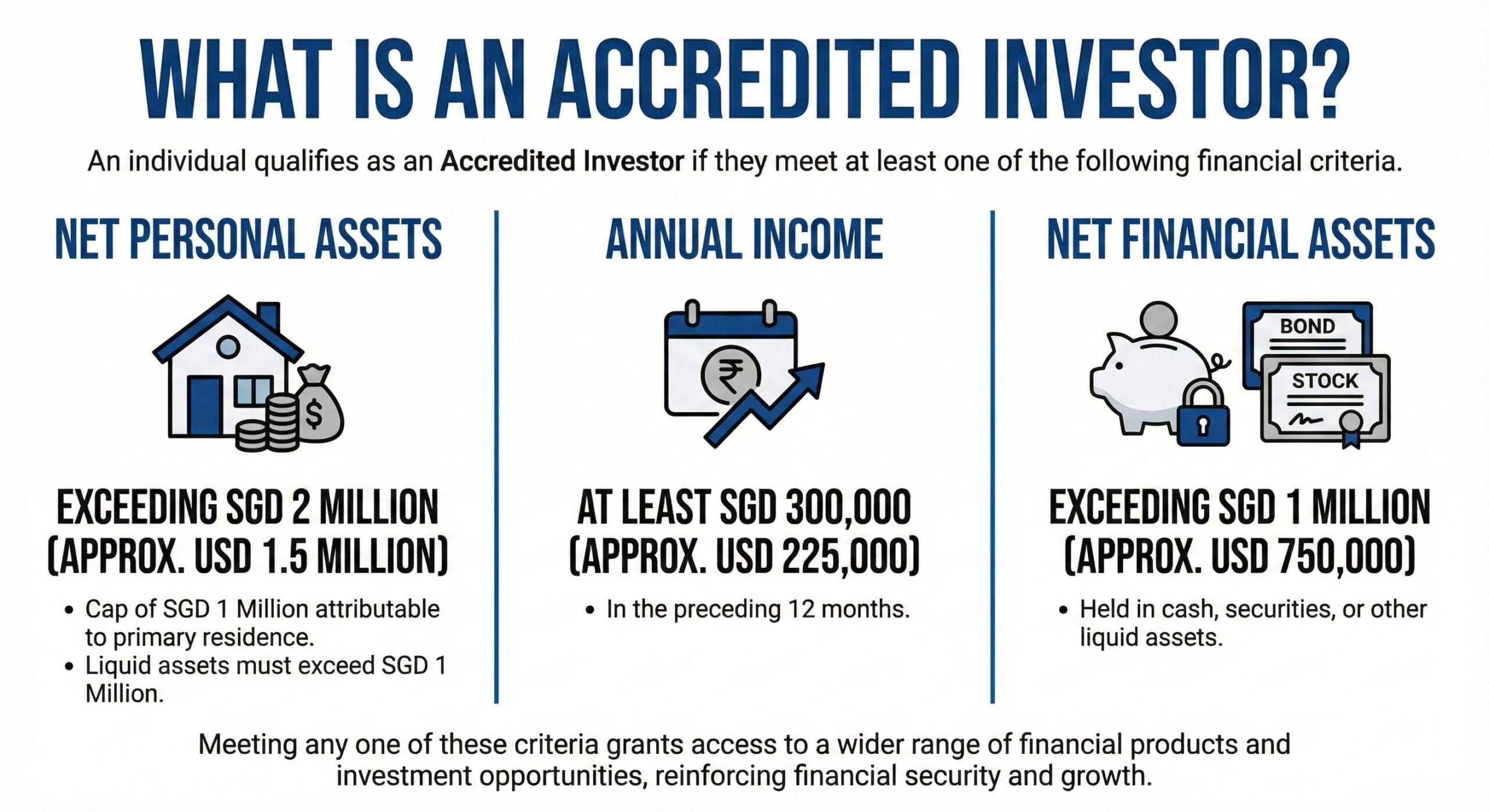

Accredited Investor Readiness

Singapore private banking often intersects with Accredited Investor classification. Meeting AI criteria does not guarantee a bank account, but it helps frame the client as a suitable wealth client rather than a retail applicant.

Individual AI route

Common criteria include net personal assets above SGD 2m, net financial assets above SGD 1m, or income of at least SGD 300k in the preceding 12 months. Banks still verify documents and may apply stricter internal standards.

Corporate or holding company route

Corporate applicants are assessed through net assets, beneficial ownership, business purpose, audited accounts, directors, signatories, transaction flows, and source of wealth behind the owners.

Family office route

Singapore can be powerful for family-office structures, but banks expect a coherent governance story, asset origin, investment policy, tax residence analysis, and clear economic purpose.

How We Prepare a Singapore Bank Account Application

The strongest Singapore applications do not start with a bank form. They start with a bankable file: identity, tax residence, wealth origin, account purpose, expected flows, and a reason the relationship belongs in Singapore.

1. Profile stress test

We identify nationality, residence, PEP, sanctions, adverse media, crypto, complex ownership, and tax-residence issues before any banker sees the file.

2. Bank route matching

We match the client to a Singapore private bank, wealth desk, or corporate banking route based on appetite and relationship value.

3. KYC dossier build

We sequence identity, proof of address, tax, source of funds, source of wealth, corporate documents, and account-purpose evidence.

4. Banker introduction

The file is positioned as a relationship opportunity, not a cold application with unexplained risk.

5. Onboarding coordination

We coordinate banker questions, certified copies, forms, video or meeting requirements, and activation steps.

Which Singapore Route Fits Your Profile?

Use this matrix to understand where your profile sits before approaching a bank. It is a commercial fit guide, not a guarantee of approval.

Strong route when assets, tax residence, and source of wealth are clean.

Works well with sale documents, cap table, tax evidence, and proceeds trail.

Reviewable when ownership, purpose, and operating history are transparent.

Possible only with exchange records, wallet history, tax reporting, and fiat trail.

Why Singapore Is Attractive for Non-Resident Wealth

Singapore is one of Asia’s deepest wealth-management hubs, with MAS reporting S$6.07 trillion in asset management AUM for 2024 and a large share of assets sourced from outside Singapore. For international clients, the appeal is not secrecy. It is institutional quality, regional market access, stable regulation, multi-currency infrastructure, and professional wealth-management depth.

| Singapore advantage | What it means for a non-resident |

|---|---|

| Asia wealth hub | Strong regional coverage for ASEAN, China, India, and global portfolio allocation. |

| MAS-regulated financial centre | Banks apply disciplined AML, KYC, and private banking controls. |

| Multi-currency banking | Useful for international investment, liquidity, and treasury planning. |

| SDIC deposit insurance | Singapore-dollar insured deposits with scheme members are protected up to S$100,000 per depositor per member, subject to scheme rules. |

Official references: MAS Singapore Asset Management Survey, MAS Accredited Investor FAQ, and SDIC Deposit Insurance Scheme.

Service Fee Schedule

Pricing depends on the complexity of the profile, not just the jurisdiction. Bank custody, investment, transfer, and product fees are separate and charged by the institution where applicable.

Standard Singapore Route

CHF 2,000

- Clean HNWI profile

- Accredited-investor ready

- USD 3m+ target relationship

Corporate / Holding Route

CHF 10,000

- Company or holding structure

- UBO and corporate KYC dossier

- Enhanced bank matching

Complex Wealth Route

Custom

- PEP, crypto, trust, foundation, or multi-jurisdictional wealth

- Enhanced due diligence

- Family-office level preparation

Frequently Asked Questions

Can a non-resident open a Singapore bank account?

Yes, but non-resident approval depends on the banking route. Private banking clients are assessed on assets, source of wealth, tax residence, nationality, account purpose, and commercial relationship value.

What is the minimum deposit for Singapore private banking?

There is no single official minimum. For our Singapore private banking route, USD 3m+ is the realistic working threshold. USD 1m-3m can be selective, while USD 5m+ usually creates stronger bank choice.

Can the account be opened remotely?

Some steps can be coordinated remotely, but Singapore private banking onboarding remains banker-led and compliance-led. The bank may require video verification, certified documents, or a meeting depending on the profile.

Do I need Accredited Investor status?

AI readiness is highly relevant for private banking and investment access. Meeting the formal AI criteria does not guarantee account approval, but it helps frame the relationship correctly.

Can a foreign company open a Singapore bank account?

It can be possible, but banks will scrutinize beneficial ownership, business activity, audited accounts, transaction flows, source of funds, and the reason Singapore is needed.

Can crypto wealth be accepted?

Crypto wealth can be reviewed only when the origin, exchange records, wallet history, fiat conversion, and tax treatment are well documented. Unsupported wallet balances are not enough.

Secure Your Singapore Banking Roadmap

Send your profile for a confidential first review. We will tell you whether the case is standard, selective, complex, or not ready before a bank application is made.