Switzerland’s 47 largest retail banks were just ranked by digital functionality — and for the third consecutive year, UBS claimed the top spot. The 2026 edition of the Institut für Finanzdienstleistungen Zug (IFZ) Digital Banking Study, published on 5 May 2026, evaluated 145 digital criteria across e-banking, mobile apps, automation, and customer communication. UBS scored highest overall. But here is what matters more for anyone choosing a bank today: mobile banking in Switzerland has officially caught up to desktop, neobanks are inside the top five of the mobile sub-ranking, and some of the country’s most recognisable cantonal banks quietly slipped out of the top tier. The rankings are useful — the gaps they reveal are more useful still.

What 145 Criteria Actually Measure — and What They Don’t

How the 145 Criteria Are Weighted: Study Category Breakdown

Source: IFZ Digital Banking Study 2026 — Punkte und Themenbloecke auf Funktionalitaetsebene

Category weights: M-Banking 15%, Touchpoints/Customer Interactions 15%, Investing & Retirement 13%, Financing 13%, Branch Digitalisation 13%, Payments 10%, E-Banking 5%, Website & General Services 4%, Automation & Process Efficiency 4%, Data Analytics & ML 3%, Adjacent Banking Services 3%, Technology Deployment 2%.

Most annual bank rankings measure customer satisfaction, branch density, or interest rates. This one measures something different: the sheer breadth of digital features a bank makes available. The IFZ study counted 145 functionalities this year — 13 more than the previous edition — spanning mobile banking, e-banking, data analytics, payment automation, digital onboarding, multi-currency support, crypto access, and virtual card issuance, among others.

That is a meaningful scope. But the methodology comes with a caveat the study is admirably transparent about: only feature availability was scored. Whether those features work well, feel intuitive, or actually serve customers is explicitly excluded from the assessment. A bank that offers 90 features with mediocre execution scores higher than one with 70 features that work flawlessly.

For most readers of a ranking like this, that distinction matters enormously. When you open a mobile banking app to make a cross-border transfer at 11pm, you don’t care whether your bank technically offers international payments — you care whether the flow is fast, the FX rate is visible upfront, and the transfer actually settles when it says it will. The study measures the menu, not the meal. Both things are worth knowing.

With that framing in place, the findings become genuinely useful rather than just impressive-sounding. Think of the IFZ ranking as a starting shortlist, not a final verdict.

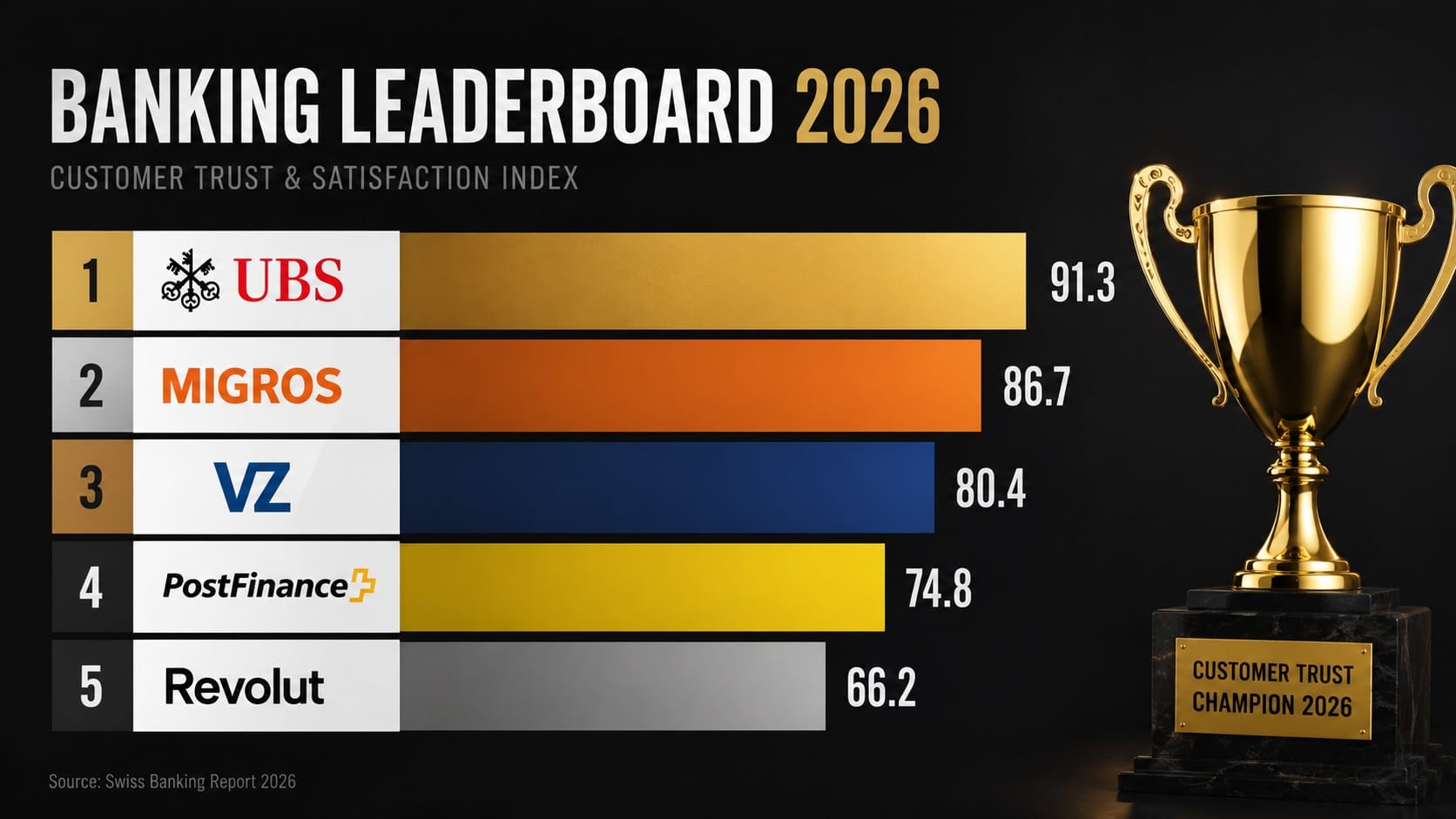

UBS Leads — But the Real Story Is the Size of the Gap Below It

UBS ranks first, followed by Migros Bank, VZ Depotbank, PostFinance, and Luzerner Kantonalbank in the overall standings. The top four positions are unchanged from 2025 — which sounds stable until you look at what’s happening across the broader field.

The study found that a significant portion of the 47 banks assessed score less than half of UBS’s total points. That is not a small gap — it is a structural divide between institutions that have committed to digital investment and those that have not. Larger institutions tend to score higher, which is predictable: they have bigger technology budgets, dedicated digital product teams, and enough customers to justify building features that only a small percentage will use. What’s less predictable is how dramatically some mid-sized banks have closed the gap.

Swissquote, for instance, entered the overall top ten for the first time. Valiant Bank moved up the rankings. Luzerner Kantonalbank broke into the top five. These aren’t brands with UBS-scale resources — they’re institutions that made deliberate, focused digital choices and built feature coverage that punches above their balance sheet weight.

The downside story is equally instructive. Raiffeisen, the St. Galler Kantonalbank, the Banque Cantonale de Genève, and Hypothekarbank Lenzburg all fell in the rankings. Most conspicuously, Zürcher Kantonalbank — a name synonymous with Swiss financial conservatism — dropped to 16th place in the unweighted ranking, out of the top 15 for the first time.

Mobile Banking Has Reached Feature Parity With Desktop — and That Is a Bigger Deal Than It Sounds

The study’s most significant structural finding is not about any individual bank. It’s about the platform shift now underway across the entire Swiss retail banking sector: mobile banking apps have, in aggregate, reached functional parity with classic e-banking portals.

For years, mobile apps were stripped-down companions to a “real” banking interface that lived in the browser. You could check your balance and make a basic transfer — but for anything complex, you were directed back to the desktop. That era is ending. The IFZ’s dedicated mobile sub-ranking (using 88 criteria assessed independently) shows that the gap between what you can do on your phone and what you can do on a computer has largely closed at the leading banks.

In the mobile-only ranking, UBS leads again, followed by Migros Bank, VZ Depotbank, and PostFinance. Revolut enters at fifth — the only non-Swiss, digital-only institution in the top five. Neon and Yuh, two Swiss neobanks that have grown rapidly among younger urban customers, both make the top 15 of the mobile sub-ranking despite not appearing prominently in the overall standings.

This tells you something worth remembering: in mobile banking specifically, a neobank with five years of history can match the feature coverage of institutions with decades of infrastructure behind them. The bottleneck is no longer heritage or size — it’s prioritisation. Banks that chose mobile-first built mobile-first products. Those that treated mobile as an extension of their web platform show it in the sub-ranking.

Neobanks vs. Traditional Banks: Where the Feature Differences Are Real

The IFZ study explicitly distinguishes between traditional retail banks and digital-only players, and the differences are worth unpacking in concrete terms rather than generalities.

Digital banks — Revolut being the clearest example in this study — lead on features that were considered experimental just three years ago: multi-currency accounts with real-time exchange, virtual card generation on demand, cryptocurrency purchase and custody within the same app, and granular spending analytics with per-category budgeting. These aren’t premium add-ons. They’re standard features of the neobank baseline offering.

Traditional Swiss banks, including some in the top 10, still have meaningful gaps in precisely these areas. A cantonal bank might offer exceptional mortgage management tools and robust investment account integration — things Revolut cannot replicate — while having no crypto access, limited foreign currency functionality, and a card management interface that requires three steps to do what a neobank does in one.

Neither model is objectively better. They’re built for different primary users. The neobank feature profile serves someone who travels frequently, earns in multiple currencies, or wants to manage spending closely. The traditional bank’s depth in investment tools, custody services, and credit products serves someone building long-term wealth in Switzerland or running a business that needs structured banking relationships.

The interesting question — which this study doesn’t yet answer — is what happens as these profiles converge. Revolut is expanding into business banking. UBS has its own digital channels team. The mid-tier is where the real competitive tension will play out over the next two to three years.

The Overperformers: What Smaller Banks Are Getting Right

The IFZ study identifies a specific group it calls “overperformers” — banks whose digital feature coverage significantly exceeds what you’d expect given their size. The 2026 list includes VZ Depotbank, Migros Bank, Swissquote, Valiant Holding, Luzerner Kantonalbank, Banque Cantonale Vaudoise, and PostFinance.

What do these institutions have in common? Each made deliberate, targeted investments in digital functionality rather than trying to build everything at once. VZ Depotbank’s entire model is built around empowered self-directed investors who want analytical tools, portfolio tracking, and trading features that rival dedicated brokers. Migros Bank, despite being a retail cooperative bank, has consistently pushed its mobile app capabilities well ahead of comparable-sized cantonal peers. PostFinance — technically a financial services arm of Swiss Post — has the distribution reach of a universal bank but the digital agility of a fintech, partly because it rebuilt its digital stack more recently than most incumbents.

There’s a lesson here that applies well beyond Switzerland. Digital overperformance in banking rarely comes from matching the biggest institution feature-for-feature. It comes from identifying your customer’s primary use case, building those features exceptionally well, and expanding from that core with discipline. The overperformers in this ranking share that focused architecture, even if they built it in very different ways.

The Study’s Biggest Blind Spot — and Why It Should Shape How You Read the Rankings

There is something important to say plainly about the IFZ methodology that the study itself acknowledges but that tends to get lost when headlines report the results: user experience was deliberately excluded. The study scored feature availability — whether a function exists — not whether it works reliably, loads quickly, requires three confusing steps, or produces clear output.

In practice, this creates a real risk of misreading the rankings. A bank that technically offers “real-time payment notifications” but sends them ten minutes after the transaction, or one that offers “investment analytics” but presents the data in a format most customers cannot interpret, scores identically to a bank that does both of those things well. The point count is the same. The customer experience is not.

This doesn’t invalidate the study — feature breadth is a genuinely useful proxy for digital investment commitment. But it does mean the ranking works best as a filter, not a decision. Banks that appear in the top 10 have demonstrated the will and capacity to build digital products. Whether any specific product in their suite works the way you need it to requires a different kind of evaluation: live app testing, reviewing user feedback, and — if you’re evaluating a bank for international transactions or multi-currency needs specifically — running a real transfer through the system before committing.

Editor’s Personal Experience — 18 Years Banking in Switzerland

I have been using Swiss banks — for both personal finance and business accounts — for eighteen years, and the gap between what the IFZ ranking captures and what daily banking actually feels like is exactly why experiential context matters alongside any study.

UBS is the clearest example. In my personal use, the mobile app has become noticeably faster over the past two years — I’d estimate around 40% quicker in load times and transaction confirmation, which sounds like a small thing until you’re approving a payment on the go.

For SME users specifically, the QR code invoice generation feature stands out. It is one of those implementations that clearly had real business owners in the room when it was designed — the flow is logical, the output is clean, and it works first time.

The geographic card blocking and spending limit controls are also more intuitive than what I’ve experienced in PostFinance, where the same functions exist but require more navigation steps and feel less immediate. None of this appears in any ranking spreadsheet — but it is exactly what you encounter when banking is part of running a business every day.

The overall visual language of the UBS app has also matured into something genuinely clear: it doesn’t try to do too much on one screen, and that restraint is what good UX looks like in practice.

What the 2026 Rankings Mean for International Banking Customers in Switzerland

For internationally mobile customers — expats, frequent travellers, cross-border workers, or anyone managing finances across more than one currency — the Swiss digital banking landscape in 2026 offers more genuine choice than at any previous point.

The entry of Revolut into the mobile banking top five is significant because it confirms that a digital-only European fintech now competes on feature breadth with Switzerland’s largest institutions in the dimension that matters most for this customer profile: the smartphone. If your primary banking needs are FX, card management, spending visibility, and fast international transfers, the neobank tier is now a fully credible option — including from within Switzerland’s regulatory perimeter.

That said, if your needs extend to mortgages, investment portfolios, pension products (3a pillar), or business accounts, you will almost certainly need a traditional Swiss bank in addition to any neobank you use. No digital-only player in the current top 15 provides the full stack of products a Swiss-resident banking relationship typically requires over time. The practical answer for most internationally oriented customers in 2026 is a two-bank model: a neobank for daily transactions and currency management, a Swiss retail bank for regulated savings products and credit. There are numerous factors to consider when looking at the top swiss private banks rankings. Each institution offers unique advantages tailored to different client needs, making it essential to assess their services thoroughly. Additionally, understanding the stability and reputation of these banks can significantly impact your banking experience in the long run.

The institutions that are likely to disrupt this two-bank norm within the next few years are the mid-tier overperformers — Migros Bank, Swissquote, and Luzerner Kantonalbank — that are building the feature breadth of digital challengers on top of the product depth of licensed banks. Watch that middle tier. The top of the ranking may be stable. The interesting movement is happening just below it.

Swiss Digital Banking 2026: Your Questions Answered

Disclaimer: This article is based on the publicly available findings of the 2026 IFZ Digital Banking Study by the Institut für Finanzdienstleistungen Zug. It is intended for informational purposes only and does not constitute financial advice or a recommendation of any specific banking institution. Product availability, app functionality, and ranking criteria may change. Always verify current offerings directly with the relevant bank before making account decisions.

Sources & References

- IFZ Digital Banking Study 2026 — Methodology & Criteria (PDF):

Institut für Finanzdienstleistungen Zug / HSLU, Punkte und Themenbloecke auf Funktionalitaetsebene 2026, published May 2026.

hub.hslu.ch — IFZ Criteria & Scoring Document (PDF) - IFZ Retail Banking Blog — Study Overview & Commentary:

Hochschule Luzern, Institut für Finanzdienstleistungen Zug, official retail banking research hub.

hub.hslu.ch/retailbanking - finews.ch — Original News Report (German), 05 May 2026:

Stefan Waldvogel, “Studie: UBS bleibt digitalste Bank der Schweiz”, finews.ch.

finews.ch — UBS bleibt digitalste Bank der Schweiz - Swiss Financial Market Supervisory Authority (FINMA) — Regulatory context:

FINMA oversees licensed banks and financial service providers in Switzerland, including digital banking authorisations.

finma.ch — Swiss Financial Market Supervisory Authority - Revolut — Corporate & Product Information:

Revolut Ltd official newsroom and product pages, referenced for neobank feature comparison.

revolut.com/news - Swiss National Bank (SNB) — Swiss Banking Sector Data:

SNB publishes authoritative statistics on Swiss retail banking, payment systems, and financial infrastructure.

snb.ch — Banks in Switzerland Statistical Publication