US estate tax for foreign investors is one of the most overlooked financial risks in international wealth management. If you are a non-US national holding American stocks, ETFs, or real estate — through a Swiss bank or anywhere else — and your US assets exceed $60,000, your heirs face a potential 40% tax bill the moment you die. No warning letter. No grace period. The assets freeze immediately upon notification of death, and the IRS gets paid before your family sees a cent.

This is not a fringe scenario. It happens to thousands of foreign investors every year. And in 2026, the compliance environment is tightening considerably.

The good news: there are four well-established strategies to eliminate — not reduce, eliminate — your exposure. Some cost nothing. Some take two weeks to implement. What matters is acting before it becomes your heirs’ problem.

Why a Swiss Bank Account Gives You No Protection

Here is a scenario that plays out regularly among international investors. A successful entrepreneur based in Zurich holds $500,000 in US blue-chip stocks — Apple, Microsoft, a broad S&P 500 ETF — managed through a private Swiss bank. The bank handles everything with discretion and precision. The account is secure. The investments are profitable. At no point does anyone at the bank mention US estate tax.

Then the entrepreneur dies.

Within days, the Swiss bank freezes the account. The heirs reach out, expecting a straightforward process. Instead, they learn the assets cannot be released without a Federal Transfer Certificate from the IRS. The estate executor must file Form 706-NA, disclosing the entire worldwide estate. The IRS claims roughly $120,000 — 24% of the portfolio — before releasing a single franc.

What follows is 12 to 18 months of frozen assets, international legal fees, and the pressure of finding liquidity from other sources just to pay a tax on money nobody can access. This is the “liquidity trap” that makes US estate tax so destructive for foreign families.

The critical misunderstanding here: the location of the brokerage account is completely irrelevant. What matters is the legal and economic location of the underlying asset. US corporation shares are classified as “US situs” assets regardless of whether you hold them through a Swiss bank, a Singapore broker, or a brokerage account in the Cayman Islands. The domicile of the asset — not the account — determines the tax liability. When investing, it’s essential to be aware of the impact of hidden charges on investments, as these can erode potential returns significantly. Many investors overlook these costs, believing that the geographical location of their accounts will shield them from unfavorable fees. However, understanding and factoring in these charges is crucial to making informed decisions that maximize investment outcomes. Investors should pay close attention to broker fees vs. irs charges, as these can have a substantial impact on overall returns. Even minor discrepancies can accumulate over time, affecting the net yield of an investment portfolio. It’s vital to conduct thorough research and seek clarity on any associated costs to ensure that your financial strategy remains robust and effective.

The $60,000 vs. $13.99 Million Gap: How the Two-Tier System Works

The United States runs two completely different estate tax regimes depending on who you are. Understanding which regime applies to you is the foundation of everything that follows.

US citizens and domiciliaries receive a federal lifetime exemption of approximately $13.99 million per person as of 2025 — effectively $27.98 million for married couples. This is why US estate tax is often called a “rich person’s tax”: it touches only the wealthiest fraction of American families.

For non-resident aliens, the exemption is $60,000. That number is not a typo. It has not been adjusted for inflation in decades. It captures virtually every foreign investor with meaningful US stock exposure. Above that threshold, the tax is progressive: 18% on the first taxable bracket, climbing to 40% on amounts exceeding $1 million.

Run the numbers and the damage becomes concrete:

| Portfolio Value (US Situs Assets) | Taxable Amount (After $60K Exemption) | Estimated Tax at Effective Rate | % of Portfolio Lost to Tax |

|---|---|---|---|

| $100,000 | $40,000 | ~$6,800 (18%) | 6.8% |

| $250,000 | $190,000 | ~$48,000 (25%) | 19.2% |

| $500,000 | $440,000 | ~$134,000 (30%) | 26.8% |

| $1,000,000 | $940,000 | ~$330,000 (35%) | 33% |

| $2,000,000 | $1,940,000 | ~$776,000 (40%) | 38.8% |

That is a significant inheritance erosion at any portfolio size above $250,000. And this happens automatically — there is no opt-out, no filing delay that prevents it, no Swiss bank privacy protection that intercepts it.

Bar chart comparing estate tax owed for a non-resident alien versus a US citizen at portfolio sizes of $100K, $500K, $1M, and $2M. US citizens owe $0 at all these values due to the $13.99M exemption. Non-resident aliens owe $6,800 at $100K, $134,000 at $500K, $330,000 at $1M, and $776,000 at $2M.

Domicile, Not Residency: The Test That Actually Matters

Here is where many advisers — including well-meaning Swiss bank relationship managers — get it wrong. The US tax code uses completely different tests for income tax and estate tax, and conflating them is expensive.

For income tax, residency follows objective criteria: the “substantial presence test” or the green card test. You can calculate your status mathematically.

For estate and gift tax, the determining factor is domicile — a subjective concept based on your intent. The IRS defines domicile as living somewhere “with no definite present intention of moving therefrom.” It is about where you consider home to be, not where you physically spent 183 days.

This distinction cuts both ways. A Swiss resident who spent several months per year in New York for business, but whose primary ties are in Zurich — family, business, property — would typically be classified as a non-domiciliary for estate tax purposes. That means the $60,000 exemption applies, not the $13.99 million one. Conversely, someone who moved to the US years ago and intends to remain permanently might be classified as a US domiciliary even without a green card. For those navigating international tax implications, understanding swiss banking options for nonresidents is crucial. These choices can provide significant advantages in managing wealth across borders. It is essential for nonresidents to consider how these banking options can affect their overall financial strategy and estate planning.

Quick caveat before we continue: this determination requires a qualified international tax attorney, not a rule of thumb. The IRS looks at the totality of circumstances. Getting it wrong in either direction has serious consequences.

What the IRS Can — and Cannot — Touch

Once you understand the domicile question, the next step is mapping your assets against the “situs rules.” These rules determine which assets fall under US estate tax jurisdiction regardless of where you live.

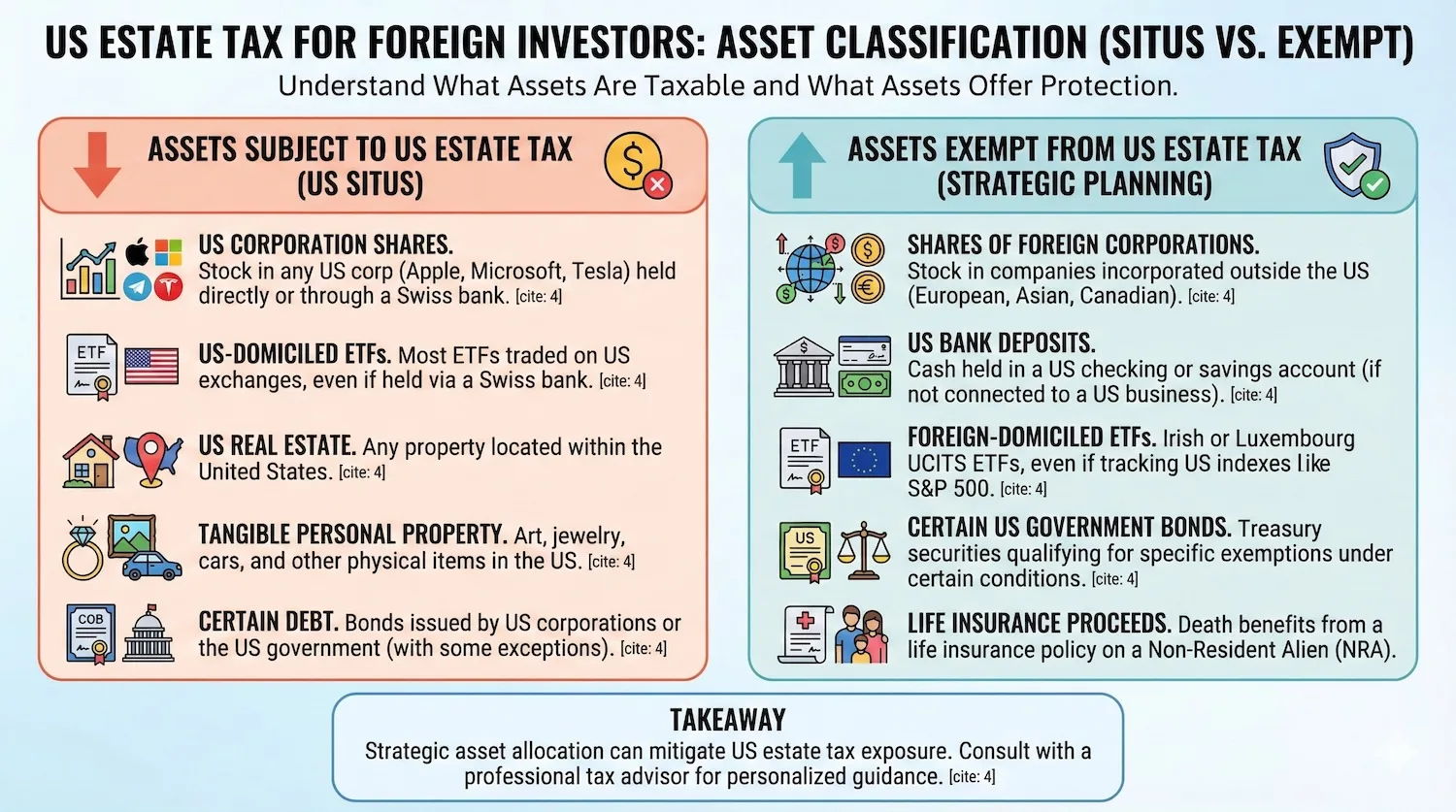

Assets That Are Subject to US Estate Tax

US corporation shares are the most common exposure for foreign investors. Stock in Apple, Microsoft, Alphabet, Amazon, Tesla — any company incorporated in the United States — is a US situs asset. It does not matter how you hold it, through which broker, or in which country your account sits. The shares themselves have US situs.

US-domiciled ETFs like SPY (SPDR S&P 500 ETF Trust) and VOO (Vanguard S&P 500 ETF) are also US situs assets. They are incorporated in the United States, so they follow the same rule as individual US stocks.

US real estate, tangible personal property located on US soil (art, jewelry, vehicles), and certain US corporate bonds also fall into the taxable category.

Assets Outside IRS Reach

This is where strategic planning becomes possible. Several asset categories escape US estate tax entirely, and understanding them opens up practical solutions.

Shares of foreign corporations are not US situs assets, regardless of what those companies own or where they invest. A share of a company incorporated in Ireland, Luxembourg, the Netherlands, or virtually anywhere outside the US is a non-US situs asset. This is the legal foundation for both the UCITS ETF strategy and the blocker corporation strategy described below.

US bank deposits — cash held in a US checking or savings account — are specifically exempted from US estate tax, provided they are not connected to a US trade or business. This exemption often surprises foreign investors who assume all US-held assets are exposed.

Foreign-domiciled ETFs (UCITS funds domiciled in Ireland or Luxembourg) fall into the non-US situs category even when they track US indices like the S&P 500 or Nasdaq 100. The fund itself is Irish or Luxembourgish. Your estate holds shares of a foreign company, not US stocks.

Life insurance proceeds from a policy on a non-resident alien are also exempt. For high-net-worth investors with significant coverage, this can be a meaningful planning component.

The US-Swiss Estate Tax Treaty: A Powerful Benefit Most Swiss Residents Miss

If you are domiciled in Switzerland, there is a treaty provision that could eliminate your estate tax liability entirely — and most Swiss bank clients have never heard of it.

The United States and Switzerland signed an estate and gift tax treaty in 1951, still in force today. The key clause allows a Swiss domiciliary to claim a pro-rata share of the much larger US citizen exemption, calculated based on the ratio of US assets to worldwide assets.

The formula works like this:

Treaty Exemption = (US Situs Assets ÷ Worldwide Estate) × US Exemption Amount

Example: $500,000 in US stocks ÷ $5,000,000 worldwide estate × $13,990,000 = $1,399,000 treaty exemption

Since $1,399,000 exceeds the $500,000 of US assets, the taxable estate is zero.

Compare that to an investor with the identical portfolio but domiciled in Turkey, India, or Singapore — countries with no US estate tax treaty. They face $440,000 in taxable estate and an estimated $134,000 tax bill. The difference between jurisdictions is not a technicality. It is $134,000.

The treaty landscape in 2026 covers only about 15 countries: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Ireland, Japan, the Netherlands, South Africa, Switzerland, and the United Kingdom. If your domicile country is not on that list, you receive zero treaty relief and the strategies below become not optional but essential.

Worth noting: even Swiss domiciliaries with large US portfolios may exceed their treaty exemption. At sufficiently high US allocations relative to worldwide assets, the pro-rata calculation still leaves taxable exposure. In those cases, the UCITS ETF switch or a blocker corporation handles the remainder.

Four Strategies That Eliminate US Estate Tax for Foreign Investors

These are not theoretical options. Each one has been used by thousands of international investors. They differ in cost, complexity, control retention, and who they suit best.

Timeline: 2–4 weeks

Control: Full

Best for: ETF investors wanting the simplest possible fix with zero ongoing complexity

Timeline: 2–6 weeks

Control: None (assets leave your estate)

Best for: Investors with clear succession intentions and comfort gifting now

Timeline: 4–8 weeks

Control: Full

Best for: Investors holding individual stocks who need ongoing control

Timeline: 8–12 weeks

Control: Delegated to trustee

Best for: Ultra-high-net-worth ($5M+ US assets) with multi-generational planning needs

Strategy 1: Switching to Irish and Luxembourg UCITS ETFs

This is the most underutilized and most straightforward solution available. You want exposure to the US stock market — you just do not want the estate tax liability that comes with US-domiciled funds. The answer: buy the same index through a fund incorporated outside the US.

Irish and Luxembourg UCITS ETFs track identical indices to their US counterparts. The iShares Core S&P 500 UCITS ETF (domiciled in Ireland) tracks the same S&P 500 index as SPY and VOO. The Vanguard S&P 500 UCITS ETF (also Irish-domiciled) does the same. Performance is nearly identical — we are talking about the same underlying index, held through a different corporate wrapper.

The difference for estate tax purposes is total. Because these funds are incorporated in Ireland under EU law, the shares are classified as non-US situs assets. Your estate holds shares of an Irish company, not US stocks. The IRS has no claim on them.

Implementation is a single transaction: instruct your Swiss bank to sell the US-domiciled ETFs and purchase their UCITS equivalents. Cost is minimal — standard trade commissions. There are no special tax consequences for making the switch within a non-retirement account. The estate tax protection is immediate once the position is established.

One real-world friction point: not all Swiss banks default to offering UCITS ETFs on their standard platforms. You may need to specifically request European exchange trading access, or work with a bank that actively supports this. Opening a Swiss bank account with international ETF capabilities built in makes this considerably easier.

Strategy 2: The Lifetime Gift of US Securities

Here is an asymmetry in the US tax code that most international investors and many advisers are unaware of. The US imposes estate tax on NRAs for US situs assets at death. But it explicitly exempts lifetime gifts of US intangible property — stocks, bonds, and mutual funds — from gift tax entirely.

NRAs are subject to US gift tax only on gifts of US-situs real and tangible property (real estate, art, jewelry). Gifts of intangible property like securities: zero gift tax.

So if you hold $500,000 in US stocks and gift them to your heirs during your lifetime, you owe no US gift tax on the transfer. When you die, you no longer own those assets. Your estate owes zero US estate tax on them. The IRS gets nothing.

The practical limit is psychological: you must relinquish control of the assets while you are alive. The gift is irrevocable. You cannot change your mind if your relationship with the intended heir changes, or if you later need the funds. For many investors, this loss of control is the dealbreaker — which is why the blocker corporation strategy exists.

Strategy 3: The Foreign Blocker Corporation

For investors who need to retain control of their US investments but want estate tax protection, the blocker corporation is the standard professional solution. You establish a non-US corporation (Ireland, the Netherlands, and Luxembourg are popular choices for treaty reasons), transfer your US stocks to the corporation in exchange for shares, and you now hold shares of a foreign company rather than US stocks directly.

Upon your death, your heirs inherit shares in the foreign corporation. Since those shares are non-US situs assets, the IRS has no estate tax claim on them. The US stocks are still inside the corporation — and the corporation pays any applicable taxes on dividends or gains — but the estate tax exposure is eliminated at the shareholder level.

Setup costs run $5,000–$8,000 for a proper Irish or Dutch structure, with annual maintenance of roughly $1,500–$2,500 for compliance and filings. Against a $500,000 portfolio facing a potential $134,000 tax, the economics are obvious. The one-time setup cost pays for itself in full the first year simply by removing the exposure.

One important caveat: the IRS will disregard a “shell” blocker corporation without substance. The structure must have a real business purpose (holding investments qualifies), maintain actual bank accounts, and file annual corporate returns. An adviser who tells you to just set up a Cayman shell with no real operations is creating a structure that could be challenged on audit.

Also: if your heirs plan to move to the US or become US citizens, the PFIC (Passive Foreign Investment Company) rules create income tax complications that need separate planning. This strategy works best when heirs are and intend to remain non-US persons.

Strategy 4: The Foreign Irrevocable Trust

For ultra-high-net-worth individuals with complex family situations, a properly structured foreign irrevocable trust offers maximum planning flexibility. You establish a trust under the laws of a foreign jurisdiction — Ireland, the UK, and Jersey are common choices — transfer your US assets to the trust, and designate beneficiaries. The trust owns the assets; you no longer do. Upon your death, the trust distributes benefits to your heirs outside the US estate tax system.

The advantages are real: professional trustee management, multi-generational planning, creditor protection, and the ability to handle complex family dynamics. The costs are also real: $15,000–$30,000 or more to establish properly, with ongoing annual fees for trustee services, tax filings, and accounting.

This strategy makes sense when you have $5 million or more in US assets, complex family circumstances, or a genuine need for the professional oversight and asset protection features a trust provides. For most foreign investors with $500,000–$2 million in US exposure, the UCITS ETF switch or blocker corporation delivers identical estate tax protection at a fraction of the cost and complexity.

Doughnut chart showing that UCITS ETF switching is the most common strategy (approx. 45%), followed by blocker corporations (30%), lifetime gifts (18%), and foreign irrevocable trusts (7%).

Cost and Timeline Comparison: Choosing the Right Strategy for Your Situation

| Strategy | Setup Cost | Annual Cost | Timeline | Retains Control? | Best Suited For |

|---|---|---|---|---|---|

| UCITS ETF Switch | $0 (trade cost only) | $0 | 2–4 weeks | Yes | ETF-based portfolios of any size |

| Lifetime Gift | $0 | $500–$1,000 (Form 709 filing) | 2–6 weeks | No | Clear succession plans, comfort gifting now |

| Blocker Corporation | $5,000–$8,000 | $1,500–$2,500 | 4–8 weeks | Yes | Individual stock holders, $200K+ portfolios |

| Foreign Irrevocable Trust | $15,000–$30,000+ | $3,000–$5,000+ | 8–12 weeks | Delegated | $5M+ US assets, multi-generational needs |

What Actually Happens If You Do Nothing: The 18-Month Timeline

Foreign investors who delay often do so because the risk feels abstract. “I’m not that wealthy,” or “My bank handles everything.” Here is what the timeline actually looks like for an unprepared estate with $500,000 in US stocks.

Why 2026 Is the Year to Act: The TCJA Sunset and IRS Modernization

The estate tax risk described in this article has existed for decades. What changes in 2026 is the enforcement environment.

The Tax Cuts and Jobs Act of 2017 temporarily increased the US citizen exemption to $13.99 million. That provision sunsets at the end of 2025, reverting the exemption to approximately $7 million adjusted for inflation. The federal government will face significant revenue pressure as more domestic estates enter the taxable range. That pressure creates incentive to maximize collection from all other sources — including foreign estates, which have historically been underpursued.

At the same time, the Common Reporting Standard (CRS) has transformed the IRS’s visibility into foreign-held US assets. Swiss banks, Singapore banks, and virtually all major international financial institutions now automatically report account information to home country tax authorities, who share it with the IRS. The era of “the IRS won’t know” ended years ago. What has changed is the IRS’s capability and motivation to act on what it knows.

If you have been putting off this planning on the assumption that the IRS is unlikely to pursue your estate, that assumption is less reliable in 2026 than at any previous point. The systems that once created practical obscurity have been largely dismantled. Tax considerations for Swiss bank clients have evolved significantly as a result.

Your 2026 Action Roadmap by Domicile

If You Are Domiciled in Switzerland

Start with the treaty. Engage a qualified international tax adviser to calculate your pro-rata exemption under the 1951 US-Swiss treaty. If your US assets represent a small enough share of your worldwide estate, you may already be fully protected. Verify this with numbers — do not assume.

If the calculation shows remaining exposure, the UCITS ETF switch is the fastest path: sell US-domiciled ETFs, buy UCITS equivalents, done. If you hold individual US stocks and need ongoing control, the Irish or Dutch blocker corporation is the professional standard. The international banking advisory process typically covers both treaty verification and structure implementation.

If You Are Domiciled Outside a Treaty Country

Turkey, Spain, Mexico, India, Singapore, the Gulf states, most of Asia and Latin America — if your domicile is not on the short treaty list, you have no relief mechanism beyond the $60,000 exemption. Every dollar above that threshold faces 18–40% tax.

The UCITS ETF switch should happen immediately for any ETF-based exposure. For individual stocks, a blocker corporation is the appropriate structure. Both solutions are available through a properly equipped Swiss or Singapore private bank. The cost of implementation is measured in weeks and a few thousand dollars. The cost of non-implementation is measured in six figures.

If You Are Planning to Move to Switzerland

Consider establishing your protective structure before you move. Non-treaty-country structures are sometimes simpler to implement while you are still domiciled outside Switzerland, before Swiss domicile creates additional tax treaty and reporting obligations. The Swiss banking and asset protection landscape rewards early planning substantially over reactive planning.

Frequently Asked Questions: US Estate Tax for Foreign Investors

Does holding US stocks in a Swiss bank protect me from US estate tax?

What is the US estate tax exemption for a non-resident alien in 2026?

Are Irish UCITS ETFs really protected from US estate tax?

Do I need to file US tax forms as a foreign investor holding US stocks?

Which countries have a US estate and gift tax treaty?

Can a foreign investor gift US stocks to heirs tax-free during their lifetime?

References

- IRS — Estate Tax for Nonresidents Not Citizens of the United States (opens in new tab)

- IRS Form 706-NA — US Estate Tax Return for Non-Residents (opens in new tab)

- US-Switzerland Estate and Gift Tax Treaty (1951) — US Treasury (opens in new tab)

- IRS — Complete List of US Tax Treaties by Country (opens in new tab)

- Irish Funds Industry Association — UCITS Regulatory Framework Overview (opens in new tab)