Quick Answer: Yes — it is possible to open a Swiss bank account as non-resident in 2026. However, you must prove a clean, documented source of wealth and pass FINMA-mandated KYC/AML checks. Minimum deposits range from CHF 0 at Dukascopy to CHF 10 million at UBS Private Wealth and Pictet. Timelines run 3–12 weeks. Swissquote and Dukascopy offer full remote onboarding. Traditional private banks generally require at least one in-person meeting.

| Key Fact | Current Status — March 2026 |

|---|---|

| Non-residents eligible? | Yes — with strict KYC/AML, documented source of wealth, and minimum deposits |

| Typical timeline | 3–12 weeks (3–6 online banks; 8–12 complex/PEP cases) |

| Remote opening | Fully online: Swissquote, Dukascopy, Sygnum, Amina. Hybrid/in-person: private banks |

| Min. deposit range | CHF 0–10K (online) → CHF 500K (accessible private) → CHF 10M+ (ultra-private) |

| Deposit protection | CHF 100,000 per client per bank (esisuisse — automatic) |

| Tax confidentiality | Ended 2017. CRS auto-reporting to 110+ countries. CARF for crypto from 2027 |

| Regulator | FINMA — Swiss Financial Market Supervisory Authority |

| Russian/Belarusian nationals | Blocked in almost all cases (June 2022 Ordinance); narrow residency exception only |

| US citizens | Severely limited (FATCA); UBS SEC-registered path and PostFinance mandate remain |

| AML risk profile | Use our free AML Risk Score Calculator before applying |

The Truth About Opening a Swiss Bank Account as a Non-Resident in 2026

For the past 15 years, my working day has revolved around one specific challenge: helping high-net-worth individuals and corporate clients find and secure the right premium Swiss banking solution for their situation. Three of those years were spent inside a FINMA-registered Independent Asset Manager in Switzerland, where cross-border client onboarding, AML compliance reviews, and bank relationship management were daily responsibilities — not abstract concepts. That institutional experience eventually led me to build something of my own. Today, I run an independent consulting firm that works directly with foreign individuals and companies across dozens of countries — matching client profiles to the right banks, preparing documentation packages, and guiding applications through compliance review from start to finish.

From both positions — institutional insider and independent advisor — I have watched hundreds of applications move through the Swiss compliance process. Some cleared in weeks. Others collapsed at the first review. Rarely did a failure come down to the client’s legitimacy. Almost every time, it came down to preparation.

What This Guide Covers and Who It Is For

This guide covers every material aspect of opening a Swiss bank account as a non-resident in 2026. Inside, you will find a 14-bank comparison with current minimum deposits, a step-by-step process with realistic timelines, a full documentation checklist, a complete fee comparison, and three detailed case studies drawn directly from my own client work.

Non-residents who benefit most from this guide fall into several clear categories. Some are entrepreneurs who have built and sold businesses and now want to diversify their assets into a politically stable currency. Others are senior professionals relocating internationally who need a reliable multi-currency banking base. Many are families managing cross-border wealth across multiple jurisdictions. A smaller group are digital asset holders seeking regulated Swiss custody solutions that no other country currently matches.

Regardless of which category fits your situation, one principle applies consistently across all of them. Swiss banks in 2026 do not primarily assess whether you are wealthy. They assess whether your wealth is explainable. That shift in emphasis — from the size of your assets to the clarity of their origin — defines the modern Swiss compliance environment. Consequently, the quality of your source-of-wealth documentation matters far more than most applicants expect.

⚠️ All data in this guide reflects conditions as of March 5, 2026. Swiss banking requirements evolve rapidly. Always verify current terms with your chosen institution before applying.

1. Why Swiss Banking Still Leads in 2026

Political Neutrality and Economic Stability

Switzerland’s constitutionally enshrined neutrality remains its most powerful financial asset. Unlike other jurisdictions, Swiss-held assets are insulated from abrupt government freezes and capital controls. This architectural stability has endured through two world wars, the 2008 financial crisis, and ongoing geopolitical turbulence.

The Swiss banking system currently manages CHF 9.4 trillion in assets across 226 licensed institutions. Switzerland maintains AAA sovereign credit ratings from Moody’s, S&P, and Fitch — all three major agencies. GDP growth reached 1.4% in 2025 and is projected at 1.6% for 2026, providing a stable macroeconomic backdrop for banking relationships.

Following the 2023 UBS acquisition of Credit Suisse, UBS became Switzerland’s sole globally systemically important bank (G-SIB). The Federal Council’s June 2025 stability package — including a public liquidity backstop — further reinforced the system’s resilience. As a result, institutional confidence in Swiss banking remains at historic highs. The next chapter is the post-Credit Suisse overhaul of UBS’s new capital requirements and what they mean for depositors.

Political Neutrality & Economic Stability

Switzerland’s constitutionally enshrined neutrality remains its most powerful financial asset. Unlike other jurisdictions, Swiss-held assets are completely insulated from abrupt government freezes and capital controls.

Architectural Stability Tested By Time

Regulatory Excellence Under FINMA

The Swiss Financial Market Supervisory Authority (FINMA) enforces one of the world’s most respected financial supervisory frameworks. All Swiss banks must implement World-Check screening — Refinitiv’s global database — to vet applicants against UN, EU, and US OFAC sanctions lists, Politically Exposed Person (PEP) registers, Economically Exposed Person (EEP) lists, and adverse media records.

When a World-Check hit occurs, banks must initiate enhanced due diligence. This process includes independent multi-source identity verification, senior management approval, detailed source-of-wealth documentation, and ongoing quarterly monitoring. These measures are non-negotiable under Swiss law.

What Swiss Banking Confidentiality Means in 2026

Swiss banking confidentiality operates under two distinct regimes. Against private third parties, bank-client confidentiality remains robustly protected under the Swiss Banking Law. It is comparable to attorney-client privilege. Unauthorised disclosure carries criminal penalties: up to six months imprisonment for unintentional breaches and up to three years for deliberate violations.

However, tax confidentiality ended in 2017. Switzerland participates in the OECD Common Reporting Standard (CRS) with over 110 countries. Banks automatically transmit non-resident account data — name, address, tax identification number, account balance, and annual investment income — to home-country tax authorities each year.

Furthermore, from 2027, the Crypto-Asset Reporting Framework (CARF) will extend automatic reporting to digital assets across 74 partner jurisdictions. Additionally, information exchange with Russia has been suspended since September 16, 2022. In short: privacy from private parties remains strong; privacy from governments has largely ended.

“The decisive factor today is not anonymity but capital quality. Your primary task is proving the legal origin of your funds.” — FINMA-Certified Banking Specialist

World-Class Wealth Management Infrastructure

Swiss banks manage 25% of all global cross-border assets under management. The total stands at CHF 2.5 trillion as of end-2025. Switzerland Global Enterprise reports that Swiss financial institutions collectively oversee CHF 4.3 trillion, with 45.5% belonging to foreign clients. This infrastructure reflects centuries of expertise in cross-border tax, legal, and compliance frameworks.

Deposit protection further reinforces security. The statutory guarantee scheme, esisuisse, protects deposits up to CHF 100,000 per client per bank. This applies automatically in any bank insolvency scenario and covers both Swiss franc and foreign currency deposits.

2. Who Can Open a Swiss Bank Account in 2026?

Eligibility to Open a Swiss Bank Account as a Non-Resident

Swiss banks welcome a broad range of international clients. However, eligibility depends heavily on your financial profile, country of residence, and source of wealth. The following categories represent the primary client groups that Swiss institutions actively serve in 2026.

High-Net-Worth and Ultra-High-Net-Worth (HNWI / UHNW) Individuals

This is the most direct path to Swiss private banking. Premier institutions such as Pictet, Lombard Odier, UBP, and UBS Private Wealth typically require minimum deposits between CHF 3 million and CHF 10 million. At these thresholds, clients access bespoke investment strategies, alternative investments, and full family office solutions. Source-of-wealth documentation must be comprehensive, audited, and independently verified.

Affluent Professionals and Entrepreneurs

Senior executives, successful founders, and international consultants with CHF 500,000 to CHF 2 million available can access mid-tier private banking. Julius Baer and Axion Swiss Bank specialise in this segment. Services include tailored lending, fiduciary arrangements, and structured investment products. Strong professional credentials and clear fund documentation are essential for approval.

Mass Affluent and Online Trading Clients

Swissquote and Dukascopy serve clients with CHF 10,000–500,000 who need investment and trading capabilities. Both banks offer fully digital onboarding for most nationalities. Multi-currency accounts, robo-advisory services, and active trading platforms are available at significantly lower cost than private banks. Swissquote currently accepts clients from CIS countries and most global jurisdictions.

Cryptocurrency and Digital Asset Holders

Sygnum Bank and Amina Bank — both FINMA-licensed since 2019 — specialise in regulated digital asset banking. Minimum crypto portfolio value: CHF 50,000 for custody services. They provide segregated cold-storage custody, multi-currency accounts including Bitcoin and Ethereum, tokenisation services, and seamless fiat-crypto conversion. Complete blockchain transaction history (12+ months) is mandatory.

EU and EEA Cross-Border Workers

G-permit holders working in Switzerland, and residents in bordering German, French, Austrian, and Italian regions, can access retail banking at PostFinance and Migros Bank. Requirements are more accessible. However, these accounts are primarily designed for everyday banking rather than complex international investment services.

Swiss Citizens Living Abroad (Auslandschweizer)

This is the easiest non-resident path by far. Swiss nationals abroad face minimal onboarding hurdles. Proof of Swiss citizenship grants access to the full spectrum of Swiss banking. Non-resident status is rarely an obstacle for this group.

Eligibility & Requirements Matrix

A comparative breakdown of Swiss banking prerequisites by client profile, capital commitment, and target institutions for 2026.

Key Restrictions: Who Faces Additional Hurdles

While many international clients are eligible, certain profiles face significant regulatory barriers. Understanding these restrictions before applying saves considerable time and protects your compliance record.

| Profile | Eligible? | Key Issue | Path Forward |

|---|---|---|---|

| Russian / Belarusian nationals | Extremely limited | June 2022 Ordinance blocks most applications | Legal residency in CH/EU/EEA/UK; zero Russian income; enhanced DD required |

| US citizens / Green Card holders | Very limited | FATCA compliance costs deter most Swiss banks | UBS SEC-registered path; PostFinance mandate; specialist guidance essential |

| FATF high-risk jurisdiction residents | Possible — with EDD | Enhanced due diligence; annual surcharges CHF 500–2,000 | Thorough SoW documentation; budget 8–12 weeks |

| PEPs and EEPs | Yes — enhanced DD | Senior management approval; quarterly monitoring; up to CHF 2,000/yr fees | Multi-layered SoW; transparent risk communication; professional introduction |

| EU/EEA cross-border workers | Yes — easier path | Retail banks preferred; limited to everyday banking | G-permit / residency proof; PostFinance or Migros Bank |

| Swiss citizens abroad | Yes — easiest path | Proof of Swiss citizenship only | Full banking access; standard onboarding |

⚠️ Important: If you are a Russian or Belarusian national, a US citizen, a PEP, or a resident of a FATF high-risk jurisdiction — do not apply without specialist guidance. Incorrect applications can negatively mark your compliance record at multiple institutions simultaneously.

3. Best Swiss Banks for Non-Residents: 14-Bank Comparison (2026)

Selecting the right bank is the single most important decision in the account-opening process. Applying to a bank whose minimum deposit, geographic restrictions, or client profile requirements do not match your situation virtually guarantees rejection. The comparison below covers the 14 most relevant institutions for non-resident clients as of March 2026.

| Bank | Min. Deposit (NR) | Remote Opening | Best For — 2026 |

|---|---|---|---|

| UBS Private Wealth | CHF 5–10M | Hybrid (video + in-person) | Ultra-HNW, family offices, global reach |

| Pictet & Cie | CHF 5M | Relationship manager | Heritage private banking, alternative investments |

| Lombard Odier | CHF 3M | In-person preferred | ESG / sustainable investing, next-gen wealth |

| Union Bancaire Privée (UBP) | CHF 3M | In-person preferred | Alternative assets, boutique investment service |

| Julius Baer | CHF 2M | Relationship manager | Emerging markets, art financing (tightened Q1 2026) |

| Axion Swiss Bank | CHF 500K | In-person preferred | Accessible private banking, EU residents, ESG focus |

| Swissquote Bank | CHF 10K | Fully online | Online trading, mass affluent, CIS/global clients |

| Dukascopy Bank | None stated | Fully online | Forex, multi-currency, digital nomads |

| Sygnum Bank | CHF 50K (crypto) | Fully online | Regulated cryptocurrency custody, tokenisation |

| Amina Bank | CHF 50K (crypto) | Fully online | Multi-currency crypto accounts, fiat-crypto bridge |

| PostFinance | CHF 1M (NR) | Online (limited) | EU border residents, basic retail only |

| Migros Bank | CHF 50K | Online (limited) | EU/EEA residents, SME |

| Zürcher Kantonalbank (ZKB) | CHF 3,500 | Online (limited) | Cantonal retail, Swiss residents preferred |

| Raiffeisen Bank Switzerland | CHF 3,500 | Online (limited) | Retail, Swiss residents preferred |

📌 Minimum deposits reflect practical thresholds for non-resident applicants in March 2026. Official published minimums may differ by account type, service level, client jurisdiction, and risk profile. Verify directly with each institution.

In-Depth Profiles: Key Banks for Non-Residents

UBS Private Wealth — Global Scale and Digital Excellence

UBS is the world's largest wealth manager, with CHF 5.2 trillion in assets under administration as of end-2025. It serves ultra-HNW and family office clients through AI-powered portfolio analytics, relationship managers in over 50 countries, and bespoke credit solutions. Following the Credit Suisse integration, UBS has significantly expanded its product range and compliance infrastructure. Preliminary applications use AI-powered document verification. A secure video interview typically follows within 48 hours. In-person meetings are preferred — but not always mandatory — for final approval.

Pictet & Cie — Heritage, Alternatives, and Family Office Focus

Pictet has operated as a partnership since 1805. It manages CHF 620 billion and maintains a strict family-office and alternatives focus unavailable at larger institutions. Services include private equity, hedge funds, and structured products with favourable access terms for existing clients. Applications typically begin through professional network introductions. Approval takes 4–6 weeks after comprehensive financial profiling and a multi-stage compliance review.

Lombard Odier — Sustainability Pioneer

Lombard Odier manages CHF 310 billion with an industry-leading ESG focus. It pioneered carbon-neutral portfolios and embeds climate considerations across all asset classes. The bank strongly appeals to next-generation investors and impact-focused families. Its digital advisory platform combines traditional relationship management with algorithmic portfolio construction. International applications are accepted, though in-person meetings are strongly preferred.

Swissquote — Best for Digital-First Non-Residents

Swissquote is Switzerland's leading online bank and the top choice for non-residents who want to open a Swiss bank account remotely. The CHF 10,000 minimum entry is accessible. The fully digital onboarding process includes video identification and typically completes in 3–6 weeks. Swissquote offers multi-currency accounts, a robo-advisory service at 0.95% per annum, active trading across global markets, and mobile banking. It accepts clients from most global jurisdictions including CIS countries.

Dukascopy Bank — Multi-Currency and Forex Specialist

Dukascopy is a FINMA-licensed Swiss bank with no stated minimum deposit. It is particularly strong for forex trading, multi-currency accounts, and clients with global nomadic lifestyles. The Dukascopy Connect app enables transfers, payments, currency exchange, and virtual card issuance entirely from mobile. Onboarding is fully remote and typically completes within 3–5 weeks for straightforward profiles.

Sygnum and Amina Bank — Regulated Crypto Banking

Both Sygnum and Amina Bank hold full FINMA banking licences specifically authorising digital asset services. Sygnum offers institutional-grade cold storage with multi-signature architecture, tokenisation of traditional assets, and comprehensive custody insurance. Amina provides multi-currency accounts combining fiat and crypto, real-time conversion, and professional trading platforms. Both institutions require complete 12-month blockchain transaction history and enhanced crypto-specific due diligence.

4. Complete Documentation Requirements — March 2026

Documentation quality is the single biggest determinant of approval speed and success. Banks cannot proceed with incomplete applications. Moreover, they typically restart the compliance review clock when supplementary documents arrive after initial submission. Prepare everything before you submit anything.

| Document | Specification | Who Needs It |

|---|---|---|

| Certified passport copy | Valid 6+ months beyond application; notarised or apostilled | All applicants |

| Secondary ID | National ID or driver's licence | High-risk / EDD cases |

| Proof of address | Utility bill or bank statement — dated within 3 months | All applicants |

| Source of Wealth (SoW) | Tax returns, business financials, sale agreements, clear narrative | All applicants |

| Employment verification | Payslips (last 3 months), HR letter, employment contract | Employed professionals |

| Audited financial statements | 2 years minimum; for business owners and entrepreneurs | Self-employed / founders |

| Business registration docs | Certificate of incorporation, articles of association | Corporate accounts |

| UBO disclosure | Full beneficial ownership chain to natural persons | Corporate accounts |

| Brokerage / investment statements | 12-month transaction history and current positions | Investors / HNWIs |

| Blockchain transaction history | 12+ months from recognised exchanges; wallet proof | Cryptocurrency holders |

| PEP/EEP risk questionnaire | Senior management approval; quarterly reviews required | PEPs and EEPs |

| Tax residency certificate | Current jurisdiction residency; supporting returns | Russian/Belarusian applicants |

Understanding Your Source of Wealth

The Source of Wealth (SoW) declaration is your most important document. It must clearly narrate how your assets accumulated, supported by independent documentary evidence. Banks in 2026 are increasingly requesting 5–10 year financial histories, particularly for clients from emerging markets or with complex business structures.

Common acceptable sources include: employment income (payslips, HR letters), business ownership (audited financials, shareholding records, sale agreements), investment returns (brokerage statements), inheritance (probate documents, estate certificates), and real estate proceeds (sale contracts, valuations). For cryptocurrency wealth, complete blockchain transaction history, exchange account statements, and proof of initial funding are mandatory.

Check Your AML Risk Profile Before Applying

Swiss banks conduct rigorous AML risk assessments on every non-resident application. Your country of residence, profession, business structure, fund origin, and transaction patterns all contribute to your risk score. A high risk score triggers enhanced due diligence, extends timelines by weeks, and can lead to rejection at many institutions. Therefore, we strongly recommend running your profile through our free AML Risk Score Calculator before submitting any application. It identifies potential red flags in advance — giving you the opportunity to address them before they become rejection reasons.

World-Check Screening: What It Means for You

All Swiss banks use Refinitiv's World-Check database to screen every applicant against global sanctions, PEP registers, EEP lists, and adverse media. A 'hit' does not automatically mean rejection. However, it triggers enhanced due diligence: multi-source identity verification, senior management approval, and ongoing quarterly monitoring. If you are a PEP, a senior executive in a politically sensitive industry, or a national of a high-risk jurisdiction, expect this process to apply to your application.

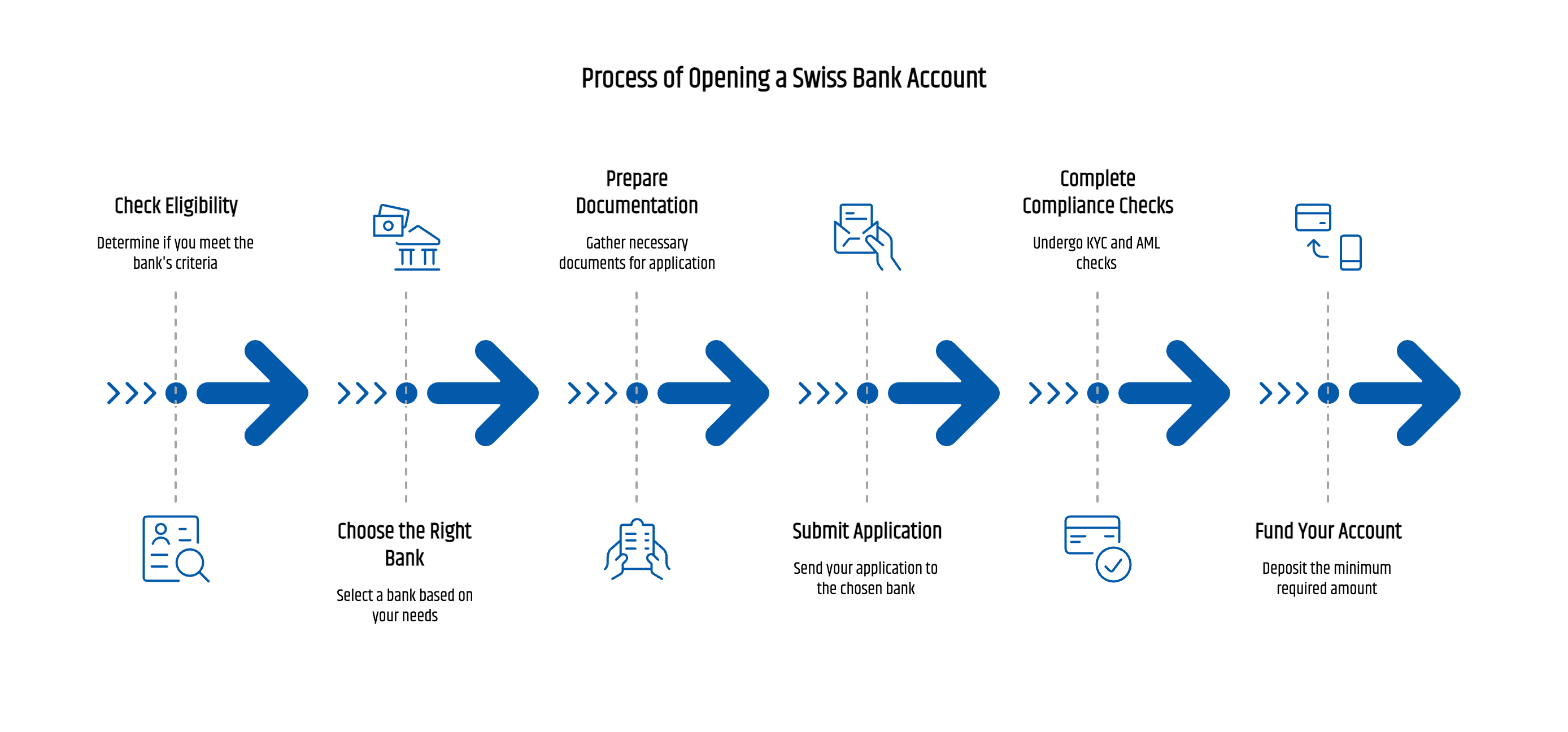

5. Step-by-Step Account Opening Process with Real Timelines

| Phase | What Happens | Duration |

|---|---|---|

| 1. Strategic Preparation | Bank research, profile matching, document assembly | 1–2 weeks |

| 2. Application Submission | Online forms, document upload, RM introduction | 1–3 business days |

| 3. KYC & Identity Validation | Video call, biometric check, World-Check screening | 2–5 business days |

| 4. Compliance & Credit Review | SoW analysis, AML check, credit committee presentation | 5–15 business days |

| 5. Approval & Account Setup | IBAN, service configuration, agreement signing | 1–3 business days |

| 6. Deposit & Full Activation | Wire transfer, card issuance, online banking access | 6–13 business days |

| TOTAL — Digital banks | e.g. Swissquote, Dukascopy | 3–6 weeks |

| TOTAL — Private banks | e.g. Pictet, Lombard Odier, UBP | 6–8 weeks |

| TOTAL — Complex cases | PEP/EEP, high-risk jurisdictions, corporate structures | 8–12 weeks |

Phase 1: Strategic Preparation — 1 to 2 Weeks

This is where most applicants underinvest — and where most delays originate. Start by matching your financial profile to bank eligibility criteria: deposit capacity, geographic restrictions, service needs, and digital versus in-person preference. Shortlist two or three institutions. Then assemble your complete document package. Obtain certified translations for any non-English, non-German, non-French, and non-Italian documents. Secure notarisations and apostille certifications where required.

A professional pre-submission audit at this stage typically saves weeks downstream. Our Swiss bank account opening service includes a full document review and bank matching consultation before you submit a single form.

Phase 2: Application Submission — 1 to 3 Business Days

Complete the bank's online onboarding forms and upload scanned documents via secure encrypted portals. For private banking clients, schedule a preliminary consultation with your assigned relationship manager. Discuss investment objectives, service expectations, and account structure. Review fee schedules and service agreements before proceeding. Having a professional introduction to the relationship manager at this stage significantly improves processing speed and approval probability.

Phase 3: KYC and Identity Validation — 2 to 5 Business Days

Banks conduct biometric facial recognition matching against passport photographs, live document authenticity verification via video call, and automated World-Check screening. PEP or EEP clients, and those from high-risk jurisdictions, trigger enhanced due diligence at this stage. Expect additional compliance interviews, senior management review, and requests for supplementary documentation.

Phase 4: Compliance and Credit Review — 5 to 15 Business Days

The bank's credit and compliance committee reviews the complete client dossier. This includes authenticating employment, business, and investment documentation; tracing cross-border fund flows for clients with complex international structures; conducting AML and counter-terrorism financing assessment; and evaluating overall credit risk. The committee can approve, request additional information, or decline. Additional information requests reset the timeline. Consequently, complete documentation on first submission is critical.

Phase 5: Approval, Setup, and Activation — 7 to 16 Business Days

Upon committee approval, you receive formal notification with account terms, fee schedules, and deposit instructions. IBAN assignment, service package configuration, and investment platform activation follow within 1–3 business days. You then wire the required minimum deposit. After AML clearance — typically 1–3 business days — full service activation including card issuance, online banking, and mobile app setup takes a further 5–10 business days.

How to Accelerate Your Swiss Bank Account Opening

- Engage a specialist for a comprehensive pre-submission document audit before applying

- Target banks with digital onboarding capabilities matched to your client profile

- Submit 100% complete documentation on first submission — partial submissions always cause delays

- Leverage professional network introductions to relationship managers, bypassing cold-application screening layers

- Prepare proactively for additional information requests — have a secondary evidence set ready from the outset

6. Swiss Bank Account Fees for non-resident clients: Full 2026 Comparison

Free accounts for non-residents are effectively non-existent in Switzerland. Every banking relationship involves multiple cost layers. Understanding them before opening an account enables accurate financial planning and effective fee negotiation.

| Bank | Monthly Fee | Non-Resident Surcharge | High-Risk Annual | Wire Transfer | Inv. Mgmt Fee |

|---|---|---|---|---|---|

| UBS Private Wealth | CHF 50–100 | CHF 50 | CHF 1,000–2,000 | CHF 20 + % | 0.5%–1.5% |

| Pictet & Cie | Negotiable | Included | Custom | Custom | 1.0%–2.0% |

| Lombard Odier | Negotiable | Included | Custom | Custom | 0.8%–1.8% |

| UBP | CHF 50–150 | Included | CHF 1,000–2,000 | CHF 25 | 0.8%–1.8% |

| Julius Baer | CHF 50–120 | Included | CHF 1,000–2,000 | CHF 20 | 0.7%–1.7% |

| Axion Swiss Bank | CHF 25–50 | CHF 25 | CHF 500–1,500 | CHF 10–30 | 0.6%–1.2% |

| Swissquote | CHF 10–25 | CHF 15 | CHF 500–1,000 | CHF 10 | 0.95% (robo) |

| Dukascopy | CHF 0–20 | None stated | N/A | CHF 5–15 | Spread-based |

High-Risk Jurisdiction Surcharges Explained

Clients classified under elevated risk categories face annual administrative surcharges on top of standard fees. These cover enhanced due diligence costs, ongoing sanctions screening, quarterly compliance review meetings, and additional administrative overhead. The surcharges apply to: FATF high-risk jurisdiction residents (CHF 500–1,500 annually), PEPs and EEPs without full family office structures (CHF 1,000–2,000 annually), ex-Russian and Belarusian nationals qualifying through the residency exception (CHF 1,000–2,000 annually), and clients with sanctions-adjacent business structures (up to CHF 2,000 annually).

Fee Negotiation Strategies That Work in 2026

- Deposit size leverage: clients depositing CHF 5M+ can often negotiate reduced maintenance fees and waived non-resident surcharges

- Service bundling: combining custody, investment management, and lending typically lowers aggregate fees versus individual service pricing

- Professional introductions: banks value referrals through established networks and frequently extend fee concessions to well-introduced clients

- Transparent risk profiling: comprehensive compliance documentation demonstrating a clean risk profile can minimise or eliminate high-risk surcharges

- Long-term commitment: expressing a multi-year relationship intention strengthens your negotiating position before account opening

7. Investment and Digital Banking Opportunities in 2026

Traditional Private Banking Investments

Swiss private banks provide access to the full investment spectrum. This includes Swiss government bonds and federal securities backed by AAA ratings (minimum CHF 10,000); diversified global equity and fixed income portfolios with professional management (CHF 100,000+ for retail clients, bespoke for family offices); private equity direct investments and fund participations (CHF 1M+ minimums); and hedge funds across long-short equity, global macro, and event-driven strategies.

Additionally, real asset exposure is available through precious metals custody, fine art financing, and structured product solutions. Swiss banks remain uniquely positioned to combine all these asset classes within a single, compliant relationship structure.

ESG and Sustainable Investing Leadership

Switzerland leads global ESG integration in banking. Lombard Odier pioneered carbon-neutral portfolios that embed climate considerations across all asset classes. Julius Baer, UBP, and Pictet integrate ESG screening criteria across traditional equity and fixed income holdings. Impact investment platforms now provide direct access to microfinance initiatives, renewable energy project finance, sustainable agriculture, and social impact bonds with measurable outcomes.

For clients who prioritise values-aligned investing, Switzerland offers an unmatched depth of institutional expertise. Furthermore, FINMA's 2026 green finance disclosure requirements are accelerating ESG integration across even smaller Swiss institutions.

Digital Banking, Robo-Advisory, and Crypto

Swissquote's robo-advisory platform manages portfolios at 0.95% per annum, with a CHF 10,000 minimum investment. AI-driven rebalancing, tax-optimised withdrawal strategies, and seamless integration with active trading accounts make it the leading digital solution for mass affluent non-residents. Dukascopy, IG Bank Switzerland, and Saxo Bank (Swiss) complement this offering with institutional-grade trading platforms.

For cryptocurrency clients, Sygnum and Amina Bank represent the most regulated and secure entry points globally. Both combine bank-grade security — multi-signature wallets, cold storage, and comprehensive insurance — with the accessibility of modern digital asset platforms. Requirements include minimum CHF 50,000 in digital assets, full blockchain transaction history, and crypto-specific enhanced due diligence.

8. Real Client Case Studies — 2026

Case Study 1: UAE Tech Entrepreneur → UBS Private Wealth

Profile: Mahmoud Al-Rashid (name changed), 34-year-old Emirati CEO of a fintech startup focused on Islamic finance. After a USD 5 million exit, he sought global asset diversification and credit facilities. Key challenges included complex source-of-wealth documentation spanning multiple funding rounds, venture capital investments, and token sales. Additionally, he required Sharia-compliant investment options within a Swiss banking framework.

Solution: A specialist compiled audited financials, cap table records, investor correspondence, and full token transaction histories before application. UBS was selected for its global digital platform, Islamic finance experience, and SEC-registered US client pathway. Remote video verification was conducted from Dubai. World-Check cleared within 48 hours due to a clean compliance profile.

Result: Private Wealth Committee approval in 5 weeks. CHF 5 million initial deposit unlocked the full private banking suite. A customised Halal-certified ESG portfolio was constructed. Credit facilities were established at competitive rates for real estate and business expansion. Quarterly strategic reviews with the UBS Middle East desk continue.

Case Study 2: UK Expat Family → Axion Swiss Bank

Profile: James and Sarah Mitchell (names changed), 52, British nationals residing in Marbella, Spain, following early retirement. They sold their London property for GBP 1.2 million and sought CHF diversification, sustainable banking, and estate planning for their two adult children.

Solution: EU residency certificates, Spanish tax returns, UK property sale contracts, and comprehensive SoW statements were prepared. Axion Swiss Bank was selected for its CHF 500K minimum, strong ESG focus, and acceptance of EU residents. An in-person consultation in Zurich established the relationship and configured a sustainable investment portfolio.

Result: Account opened in 6 weeks. CHF 600,000 initial deposit. ESG-focused portfolio generating 6% annual returns. A family trust structure was established for tax-efficient wealth transfer. Reduced maintenance fees were negotiated through a long-term relationship commitment.

Case Study 3: Singapore Digital Nomad → Swissquote Bank

Profile: Lisa Wang (name changed), 29-year-old Singaporean software developer working remotely for multiple international clients. She held SGD 500,000 in savings and needed fully digital account opening, active trading across time zones, and business banking integration.

Solution: Swissquote's fully online onboarding with video identification. Multi-currency trading platform activated. Business banking features established for freelance income alongside personal investment accounts. No Swiss visits or in-person meetings were required at any stage.

Result: Complete activation in 3 weeks. CHF 100,000 equivalent initial deposit. Commission rate of 0.15% per trade. Integrated robo-advisor managing long-term portfolio alongside active trading. Seamless global mobile banking across multiple countries.

9. Common Mistakes and Proven Success Strategies

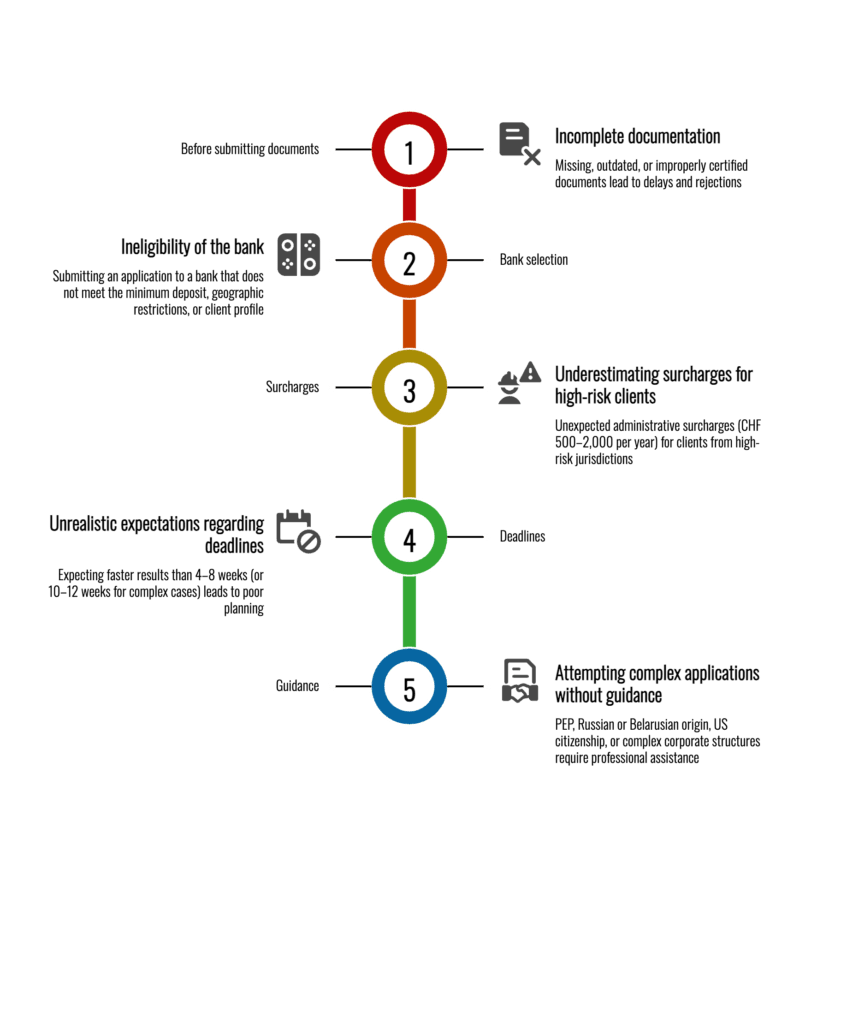

Five Critical Mistakes That Cause Rejections of non-resident account applications

Mistake 1: Incomplete Documentation at Submission

This is the most common cause of delays and rejections. Missing, outdated, or improperly certified documents halt the process entirely. Furthermore, banks typically restart the compliance review clock when supplementary documents arrive weeks after initial submission. Fix: conduct a full documentation audit before submitting anything.

Mistake 2: Mismatched Bank Selection

Applying to a bank whose minimum deposit you cannot meet, whose geographic restrictions exclude your jurisdiction, or whose client profile you do not match virtually guarantees rejection. Fix: research eligibility criteria thoroughly before applying. Target institutions genuinely suited to your specific situation.

Mistake 3: Underestimating High-Risk Surcharges

Clients from elevated-risk jurisdictions often apply without budgeting for CHF 500–2,000 in annual administrative fees. These are non-negotiable at many institutions. Fix: factor these surcharges into your long-term cost projections. Negotiate fee structures upfront where possible.

Mistake 4: Unrealistic Timeline Expectations

Swiss banks require 4–8 weeks minimum for proper compliance review. Expecting faster results leads to poor planning. Fix: apply well in advance of any funding deadline. Build buffer time for potential additional information requests. Complex cases routinely take 10–12 weeks.

Mistake 5: Attempting Complex Applications Without Guidance

PEP status, Russian or Belarusian origin, US citizenship, and complex corporate structures all require specialist navigation. Fix: engage a professional banking consultant for documentation review, bank matching, and relationship manager introductions. Our Swiss bank account opening service handles all five of these areas for international clients.

Five Strategies That Maximise Approval Probability

- Conduct a mock compliance review before formal submission — identify red flags, documentation gaps, and narrative inconsistencies early

- Gain direct relationship manager introductions through professional networks — this bypasses cold-application screening layers entirely

- Communicate transparently about your compliance posture, fund sources, and business activities upfront — proactive disclosure builds trust

- Negotiate fee structures before signing — leverage deposit size, service bundling, and long-term commitment

- Maintain meticulous ongoing documentation — provide timely updates on material changes to preserve your banking relationship

10. Future Trends in Swiss Banking: 2026 and Beyond

Blockchain-Based Digital Identity Verification

Several major Swiss banks are piloting blockchain-based digital identity systems in 2026. These store encrypted credentials on permissioned ledgers and enable instantaneous KYC verification across multiple financial institutions. Early adopters benefit from materially faster account opening and significantly reduced documentation requirements. Full deployment is expected across leading institutions by 2027–2028.

Artificial Intelligence in Compliance and Wealth Management

Swiss banks are deploying AI for real-time portfolio risk assessment, automated rebalancing, tax-loss harvesting for international clients, and behavioural analysis. Additionally, AI-driven automated compliance monitoring is reducing the manual overhead of ongoing AML requirements — a development that will ultimately reduce costs for non-resident clients with clean profiles.

CARF: Cryptocurrency Reporting Begins in 2027

The Crypto-Asset Reporting Framework (CARF) — adopted by Switzerland following the Federal Council's decision of May 2024 — extends automatic information exchange to digital assets from 2027. The first exchange involves 74 partner jurisdictions. Consequently, cryptocurrency holders with Swiss accounts must ensure home-country tax compliance for all digital asset holdings well before this deadline.

Expanded Cross-Border Regulatory Cooperation

Swiss authorities are negotiating enhanced tax information exchange agreements beyond the current OECD framework. These extend to Middle Eastern financial centres, Asian regulatory authorities, and emerging market jurisdictions. Therefore, non-resident clients should anticipate expanding reporting obligations. Proactive cross-border tax planning with qualified advisors is increasingly important.

Sustainable Finance Takes Centre Stage

FINMA's 2026 green finance disclosure requirements are driving ESG integration across Swiss banking. Reduced custody fees for sustainable investment products, enhanced climate risk reporting standards, and new green bond platforms are differentiating institutional offerings. Switzerland is consolidating its position as the global capital of sustainable private banking.

11. Frequently Asked Questions — Open a Swiss Bank Account (2026)

Conclusion: Your Roadmap to Open a Swiss Bank Account in 2026

Switzerland remains the global standard for financial stability, asset protection, and wealth management expertise. To open a Swiss bank account as a non-resident in 2026, you need three things above all others: a thoroughly documented source of wealth, the right bank matched to your profile, and realistic expectations about timelines and costs. Navigating the complexities of banking regulations is crucial for success. Implementing secure Swiss bank approval strategies can significantly enhance your chances of a smooth application process. Understanding the specific requirements of the chosen financial institution will provide clarity and increase your confidence in managing your wealth in Switzerland.

The regulatory complexity that deters unprepared applicants creates a structural advantage for those who approach the process correctly. FINMA-backed institutional resilience, CHF 100,000 deposit protection, access to global investment markets, and 25% of all global cross-border assets under management make Swiss banking worth pursuing — when pursued strategically.

Before you apply, take two important steps. First, use our free AML Risk Score Calculator to identify any compliance risk factors in your profile. Second, review our Swiss bank account opening service to understand how we support non-residents through every stage — from bank selection and documentation preparation to relationship manager introductions and ongoing compliance support.

The keys to success are consistent across all client profiles: prove the legal origin of your funds, submit complete documentation on the first attempt, target institutions genuinely suited to your situation, and engage expert guidance whenever complexity arises.

✅ Ready to open a Swiss bank accoun as non-resident? Start with our AML Risk Score Calculator — then contact our team via our Swiss bank account opening service page for a personalised bank matching consultation.

Disclaimer: This guide reflects conditions as of March 5, 2026. Swiss banking requirements evolve rapidly. All information should be verified directly with the relevant institution or a qualified Swiss banking advisor before taking action. This document does not constitute financial, legal, or tax advice.