Most freelancers who obtain Spain’s Digital Nomad Visa have two banking problems. They are aware of the first one — opening a Spanish account for rent, taxes, and autónomo registration. They are almost never aware of the second: what Spanish tax residency does to the offshore accounts they already hold.

Many nomads compare Spain with Asia because a Singapore non resident bank account can solve the operating-account problem without pretending residency alone is enough.

We work on the second problem. At Easy Global Banking, we regularly help clients who have moved to Spain on the DNV and are sitting on a US brokerage account, a Swiss private account, or a Singapore relationship they built before relocating — and who are now realising that becoming a Spanish tax resident changes the rules on all of it. This guide addresses both problems together, because solving one without the other is how people end up with expensive surprises from Hacienda.

The Autónomo Banking Problem: Straightforward, but Full of Traps

Before addressing the offshore layer, the operational Spanish account needs to work properly. It doesn’t, for most new DNV arrivals, for one consistent reason: they follow the forum advice to open N26 or Wise first, then discover neither works for Seguridad Social contributions.

Registering as autónomo requires a Spanish IBAN that Seguridad Social accepts for direct debit. Wise’s IBAN is Belgian-issued and rejected. Revolut faces the same problem. N26 results are variable, with more rejections reported in 2025 and 2026 than in previous years. The banks that reliably work are BBVA, Santander, Sabadell, and CaixaBank — all require in-branch opening, all accept a passport plus NIE certificate before your TIE arrives.

The practical sequence: go to BBVA or Santander in the first week, bring your passport and NIE certificate, open as a non-resident, and tell them you will register as autónomo. You update to resident status once the TIE comes through. Do not delay this for the fintech accounts — they come later and serve a different purpose entirely.

A client arrives in Spain, opens a Wise account the same day because it requires no branch visit, sends their first invoice to a US client, receives payment. Then they try to register as autónomo and their gestor tells them they need a traditional Spanish IBAN. They then have to open a second account — losing two to three weeks. If they are close to the six-month Beckham Law window, that delay matters.

🏦 Traditional Spanish Banks (BBVA / Santander / Sabadell)

📱 Fintech (Wise / Revolut / N26)

Traditional banks are essential for autónomo obligations but poor for FX. Fintech is excellent for currency conversion but cannot handle tax or Social Security payments.

The Offshore Banking Problem: What Spanish Tax Residency Actually Does to Your Existing Accounts

This is where the standard nomad banking guide ends and where the real problem begins for most of our clients.

A DNV holder who spends more than 183 days in Spain in a calendar year becomes a Spanish tax resident. That status change has immediate consequences for any offshore account they already hold — Swiss, Singaporean, US, British, or otherwise — regardless of whether they ever move a single euro through Spain.

Three specific things happen, and almost nobody explains all three clearly:

First, CRS reporting begins. Spain is a signatory to the OECD Common Reporting Standard. Every financial institution in every participating jurisdiction — Switzerland, Singapore, Liechtenstein, Luxembourg, the UK, the Cayman Islands — is legally required to identify account holders who are Spanish tax residents and report their balances, interest, dividends, and proceeds to the Spanish Tax Agency (Hacienda) automatically, once per year. This isn’t theoretical. It happens. If you hold a Swiss account at UBS or a Singapore account at DBS and you become a Spanish tax resident, Hacienda already knows the account exists and its approximate value. The report lands before most people have filed their first Spanish tax return.

Second, Modelo 720 may apply. Any category of foreign assets — bank accounts, investment accounts, or property — exceeding €50,000 in value must be declared to Hacienda via Form 720 by March 31 of the following year. This is separate from paying tax. It is an informational declaration. The consequences of not filing when you should have are serious: reformed penalties remain, and inconsistencies between your CRS-reported balances and your Modelo 720 filing are one of the most common triggers for a Hacienda review.

Third, foreign income becomes taxable in Spain. Under standard Spanish tax residency, worldwide income is taxable in Spain. The interest accruing on your Swiss savings account, dividends from your US brokerage, rental income from a property in London — all of it comes into the Spanish tax base under progressive IRPF rates that reach 47% in most regions.

A client contacted us after his first full year as a Spanish tax resident under the DNV. He had a US brokerage account with approximately $620,000 in assets and had received around $18,000 in dividends and capital gains during the year. He had not filed Modelo 720. He had not declared the foreign income. He had assumed — wrongly — that because the money “stayed in America,” Spain had no claim on it. By the time we spoke to him, he was facing a voluntary disclosure situation, not a planning conversation.

The Beckham Law — and Why It Changes Everything for Offshore Accounts

If there is a single most important financial decision for a DNV holder with substantial offshore assets, it is whether they qualify for Beckham Law and whether they apply for it in time.

The Beckham Law (officially the Régimen Especial para Trabajadores Desplazados, Article 93 LIRPF) does two things that matter enormously to anyone holding a Swiss, Singapore, or US account. But before getting to those, one prerequisite is frequently missed: to qualify, you must not have been a Spanish tax resident during any of the five calendar years immediately before your move. This was reduced from ten years by the 2023 Startup Law. Short tourist visits do not count as tax residency, but if you previously lived and worked in Spain for an extended period, eligibility needs to be checked carefully.

It exempts foreign-source passive income from Spanish tax. Dividends, interest, capital gains, and rental income earned from assets outside Spain are generally outside the Spanish tax base under Beckham. The 24% flat rate applies to employment or freelance income earned in Spain — the offshore investment portfolio continues to grow without Spanish tax exposure during the regime. Two important qualifications: first, this exemption applies to Spanish tax only. Your home country may still tax that income under its own rules — a US citizen, for example, still files a US return and owes US tax on global income regardless of Beckham status. Second, because Beckham taxes you as a non-resident under IRNR rules, access to Spain’s double tax treaties is generally limited or unavailable. For taxpayers with complex international income structures, this can be a meaningful trade-off that needs to be modelled before assuming Beckham is the right choice.

It waives the Modelo 720 obligation while the regime applies. Beckham Law holders are generally not required to file Form 720 for the years the regime is in force. This is a significant compliance advantage. A DNV holder with a CHF 800,000 Swiss account and a US brokerage generally does not need to declare either to Hacienda while Beckham applies. One important caveat: this exemption is personal. It does not automatically extend to a spouse who qualifies as an ordinary Spanish tax resident — they may face Modelo 720 obligations independently. The moment the main holder’s regime ends — after six years — both reporting and full worldwide income taxation return.

The catch most people hit: the Beckham Law’s standard qualifying profile is a remote employee on formal foreign payroll, not a freelancer invoicing clients as an autónomo. The 2023 Startup Law extended Beckham in principle to DNV holders, but in practice approval is much harder for standard autónomos than for employees. A DNV holder who is a salaried employee of a US or UK company with a formal employment contract has a strong Beckham case. A freelancer billing monthly invoices to multiple clients has a significantly harder one. The line isn’t always clear, and we consistently see cases where structuring the employment relationship before the DNV is applied for makes the difference between qualifying and not.

One deadline that admits no exceptions: Form 149 (the Beckham application) must be filed within six months of registering with Spanish Social Security. Miss it by one day, and Beckham is gone for the entire duration of your Spanish residency. We have seen clients lose it by waiting for a gestor appointment that ran slightly late. The six-month window starts from Social Security registration, not from the date you arrived in Spain or obtained your visa.

A note that most guides skip: Beckham is not automatically the right choice for every DNV holder. At income levels below approximately €40,000–45,000 per year, standard IRPF with the €5,550 personal allowance, autónomo Social Security deductions, and other available deductions can result in an effective rate lower than Beckham’s flat 24%. The bar chart below makes this visible. If your income is at the lower end of the DNV threshold, run the comparison with your gestor before applying — choosing Beckham irrevocably locks you out of those allowances for six years.

At €50k, standard IRPF is approximately €13,000 versus Beckham at €12,000 — a minimal difference; standard IRPF may be lower once personal allowances and deductions are applied. At €80k, standard IRPF is approximately €25,000 versus Beckham at €19,200, a saving of roughly €5,800. At €120k, standard IRPF is approximately €43,000 versus Beckham at €28,800, a saving of roughly €14,200. Figures are for Madrid; regional rates vary. Excludes Social Security contributions.

* Illustrative estimates for Madrid, single filer, after €5,550 personal allowance on standard IRPF. Beckham Law does not allow this personal allowance. At incomes below approximately €40,000–45,000, standard IRPF with allowances and autónomo deductions can result in a lower effective rate than the 24% Beckham flat rate. Regional surtaxes not included. Social Security contributions excluded. This is not tax advice — model your specific situation with a qualified Spanish tax advisor before applying for Beckham.

CRS and Your Offshore Account: What Spain Already Knows

Common Reporting Standard deserves more attention than it gets in DNV banking discussions. Understanding it determines how you approach your offshore account from the moment you register as a Spanish tax resident.

Under CRS, financial institutions in participating countries collect tax residency information from all account holders. If you hold an account in Switzerland and you tell the bank you are resident in Spain — or if they determine residency through other means — they will report your account balance, income received, and proceeds to Hacienda each year. Switzerland, Singapore, Liechtenstein, Luxembourg, the UK, Cayman Islands, and over 100 other jurisdictions participate. The US does not participate in CRS (it runs its own equivalent, FATCA), but US institutions still report to Spain under bilateral exchange agreements.

Practically, this means that if you become a Spanish tax resident and fail to declare your foreign accounts on Modelo 720, Hacienda may already have the data from the CRS report before you file. The mismatch between what the bank reported and what you declared — or didn’t declare — is exactly the kind of inconsistency that triggers a review.

Where Beckham Law provides genuine relief: during the six years the regime applies, Modelo 720 does not need to be filed. If you hold the account at a Swiss or Singapore institution during the Beckham years, the bank will still report to Spain under CRS, but because Modelo 720 is not required for Beckham holders, there is no filing inconsistency. The obligation and the exemption are aligned. After Beckham ends, Modelo 720 returns — and by then your offshore assets may have grown considerably. Planning the transition before year six is essential, not optional.

Clients who contact us before relocating to Spain — rather than after — have a planning window that clients who contact us post-move do not. A client who relocates in January and registers for Social Security in February has until August to file Beckham. Within that window, there is time to review the offshore account structure, confirm which assets are held where, and brief the Spanish gestor on the full picture before any Hacienda filings are made. Clients who contact us in month five are cutting it close. Clients in month seven have already lost the Beckham option and are starting from a much worse position.

The Banking Stack for DNV Freelancers — Built Around Your Actual Asset Picture

The optimal account structure for a DNV freelancer with non-EU income depends on two variables: the size of the income stream and whether meaningful offshore assets (savings, investments, property) exist alongside it. These are two different problems with different solutions. One option for managing these assets is to consider offshore accounts in the Caribbean, which can provide tax advantages and greater privacy. Additionally, these accounts may offer access to international investment opportunities that are not available in the freelancer’s home country. It is crucial, however, to ensure compliance with local and international regulations when utilizing such financial tools.

Five steps: map offshore assets and get tax advice before Social Security registration; open traditional Spanish bank in week one; keep home-country account and route income via Wise; file Beckham Law within 6 months; plan offshore asset restructuring before Beckham expires.

When You Need an Offshore Account — and When You Don’t

Not every DNV holder needs a Swiss or Singapore account opened specifically for Spain. But most already hold some form of offshore account — a US 401(k), a UK ISA, a home-country savings account, or a brokerage — and the question is whether to keep it, restructure it, or simply manage it within the Spanish compliance framework.

Our view on this: the DNV framework is well-designed for income-generating freelancers whose wealth is primarily in the form of active freelance income. The complication arises when accumulated assets are significant. A DNV holder with €80,000 per year in freelance income and €50,000 in savings has a different problem than one with the same income and a CHF 1.2 million Swiss account. The latter needs a properly structured offshore banking relationship — one that is CRS-compliant, documented with clean source-of-wealth records, and reviewed by a Spanish tax advisor alongside the Swiss relationship manager — before Spanish tax residency begins, not after.

For clients in that second category, the DNV is not just a visa decision. It is a cross-border wealth structuring event. The Spanish Hacienda will receive CRS data from Switzerland or Singapore automatically. The only question is whether that data lands in a context where the account is properly declared, the income correctly reported, and the Beckham exemption in place — or whether it arrives as a surprise.

| Account Type | CRS Reporting to Spain? | Modelo 720 Required? | Income Taxable in Spain? | Under Beckham Law? |

|---|---|---|---|---|

| Swiss private bank account | ✓ Yes — automatic | If >€50k aggregate | Interest: yes (progressive IRPF) | Modelo 720 waived; income generally exempt |

| Singapore brokerage / private bank | ✓ Yes — automatic | If >€50k aggregate | Dividends / gains: yes | Modelo 720 waived; income generally exempt |

| US brokerage (IBKR, Schwab, Fidelity) | ✓ Via FATCA / bilateral treaty | If >€50k aggregate | Dividends / gains: yes (Spain-US DTA applies) | Modelo 720 waived; income generally exempt |

| US 401(k) / IRA | ✓ Reported under FATCA | If >€50k — complex treatment | Complex — Spain-US DTA and pension rules apply | Specialist advice required |

| UK ISA | ✓ Yes — UK in CRS | If >€50k aggregate | Not tax-free in Spain — income is taxable | Modelo 720 waived; income generally exempt |

| Home-country current account (operational) | ✓ Yes — if country in CRS | If >€50k aggregate across all bank accounts | Interest only — typically minimal | Modelo 720 waived while regime applies |

The 20% Spanish Income Rule: Accounting for It in Your Banking Structure

The DNV requires that at least 80% of your income originates from non-Spanish clients or companies. This is an immigration compliance rule that interacts directly with how you structure your invoicing and bank accounts.

The practical enforcement mechanism is your bank statements. At DNV renewal — and potentially during Hacienda reviews — the question is whether your income split is documented clearly. The cleanest approach is the one that makes the answer obvious without reconstruction: non-EU clients pay to your home-country account (or directly to your Spanish account if you prefer), Spanish clients pay to your Spanish IBAN. A gestor looking at your monthly bank statements can calculate the 20% split immediately without opening a spreadsheet.

Where people go wrong: routing all income through one account because it’s simpler. It is simpler — until you need to demonstrate compliance and everything has to be separated from invoice records post-hoc. For autónomos with gestores filing quarterly, a clear income split in the bank data makes each quarter take half the time.

One subtlety the forums don’t mention: the 20% cap applies to the calendar year, not to individual quarters. A quarter where Spanish clients represent 30% of revenue is not automatically a violation if the annual total stays below 20%. Monthly tracking is what lets you manage this in real time rather than discovering a problem at year-end.

Bank Statements, Physical Stamps, and the 2026 Update

One operational detail that caught several of our clients off guard in 2025 and 2026: the UGE (Unidad de Grandes Empresas y Colectivos Estratégicos), which processes DNV applications, now expects bank statements submitted as income evidence to carry a physical bank stamp confirming authenticity. PDF downloads from internet banking portals are being rejected with increasing frequency.

This applies both to the initial DNV application and to renewal. If you are submitting offshore account statements — a Swiss account, a US brokerage statement — alongside your Spanish IBAN statements, ensure each document is either stamped by the issuing institution or accompanied by a letter confirming authenticity. Swiss private banks can typically provide this on letterhead. US brokerages sometimes require a formal request to their client services team. Build two to three weeks of lead time into any application timeline that requires foreign bank documentation.

Related reading:

Frequently Asked Questions

Does Spain automatically receive information about my Swiss or Singapore bank account? +

Yes. Both Switzerland and Singapore participate in the OECD Common Reporting Standard. If your bank identifies you as a Spanish tax resident — which they are required to do through annual self-certification — they will report your account balances, interest, dividends, and redemption proceeds to their domestic tax authority, which then forwards the data to Hacienda. This happens once per year, covering the prior calendar year. The report typically reaches Hacienda before most clients file their annual Spanish tax return. Failure to declare an account that Hacienda already knows about from CRS data is one of the more common triggers for a formal inquiry.

Do I need to close my offshore account when I move to Spain on the DNV? +

No — and closing it is usually the wrong move. Your home-country account is the collection point for non-EU client income and the foundation of the income paper trail that DNV renewal requires. What changes when you become a Spanish tax resident is your reporting obligation: depending on the account value and whether you qualify for Beckham Law, you may need to declare it on Modelo 720. The account itself is not problematic. An undeclared account above the threshold, or income from it not reported to Hacienda when required, is the issue. Proper structure and timely declaration resolve this — account closure does not.

Can I use Wise as my primary account for autónomo tax payments? +

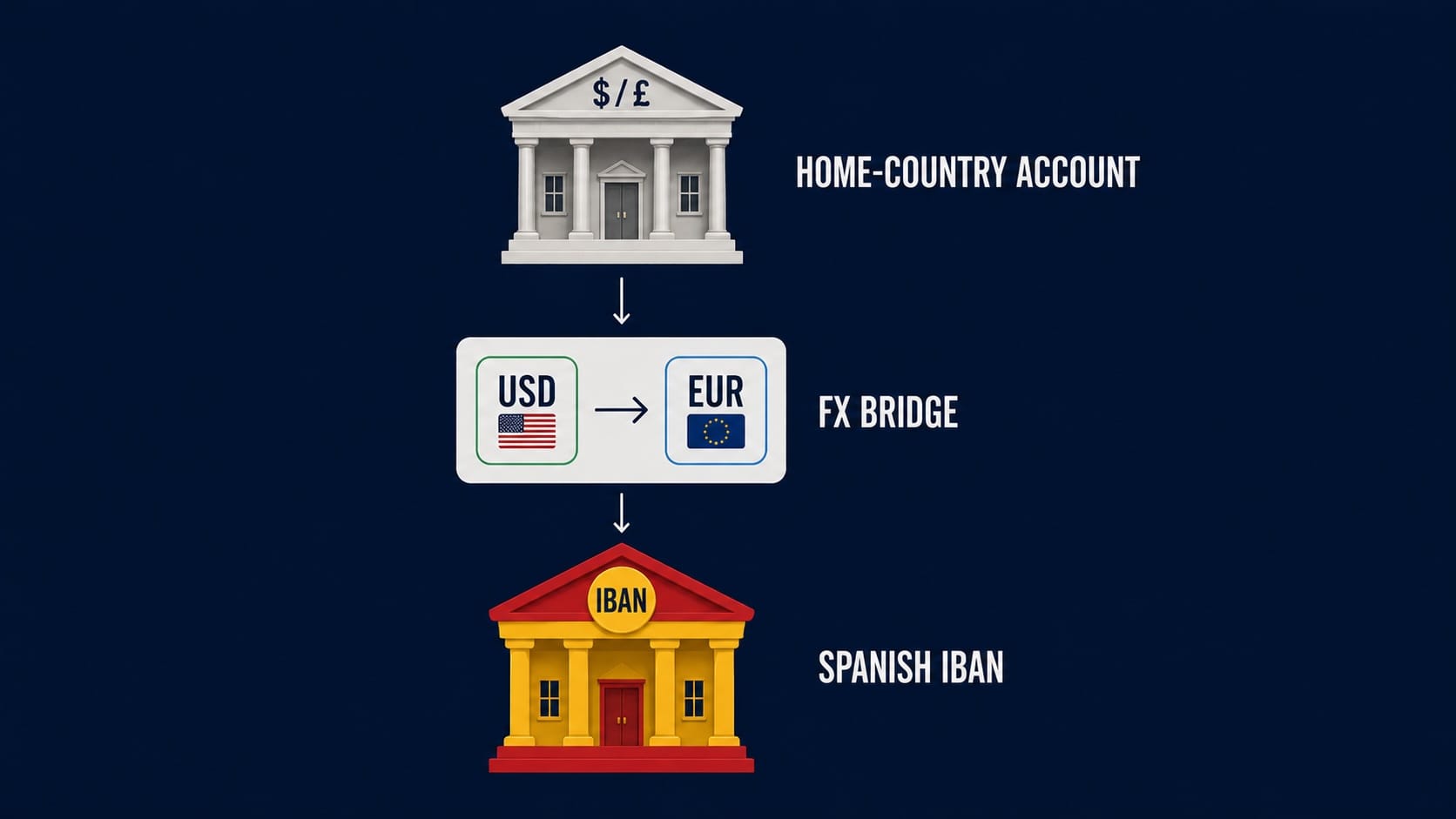

No. Wise’s IBAN is issued by a Belgian institution and is consistently rejected for Seguridad Social direct debit payments. Revolut faces the same issue. For autónomo registration and all Spanish tax and social security payments, you need a traditional Spanish IBAN from BBVA, Santander, Sabadell, or CaixaBank. Wise has a specific and valuable role in the banking stack — converting non-EUR income from your home-country account to EUR at near mid-market rates before sending to your Spanish IBAN. It is a currency bridge, not an autónomo operating account.

Does the Beckham Law exempt me from declaring my foreign bank accounts? +

Yes — while the regime applies, and with two qualifications. Beckham Law holders are generally exempt from Modelo 720 because they are taxed under IRNR (non-resident) rules rather than as standard Spanish tax residents. This exemption is personal: it does not automatically extend to a spouse who is separately a standard Spanish tax resident, who may face Modelo 720 obligations independently. Additionally, because Beckham holders are treated as non-residents for income tax purposes, access to Spain’s double tax treaties is generally limited or unavailable — a consideration for anyone with US, UK, or other treaty-dependent income structures. Both the Modelo 720 exemption and treaty access should be verified with a qualified Spanish tax advisor for your specific situation.

Can freelancers on the DNV qualify for Beckham Law? +

In principle yes, following the 2023 Startup Law. In practice, standard autónomos invoicing multiple clients directly face significant approval difficulties. The strongest Beckham profiles for DNV holders are remote employees on formal employment contracts with a foreign company. Three further points worth knowing: (1) You must not have been a Spanish tax resident during any of the five calendar years immediately before your move — this was reduced from ten years by the Startup Law. (2) At lower income levels (roughly under €40,000–45,000/year), standard IRPF with personal allowances and autónomo deductions can produce a lower effective rate than Beckham’s 24% flat — so Beckham is not automatically advantageous. (3) Beckham holders are taxed as non-residents under IRNR rules, which generally removes access to Spain’s double tax treaties. Model your specific income structure before deciding.

What is the Modelo 720 threshold and which accounts count toward it? +

Modelo 720 groups foreign assets into three categories, each with a separate €50,000 threshold. Category one covers all foreign bank and deposit accounts — your Swiss account, your US checking account, your Wise balance held in foreign currency, and your Singapore account all count together. If their combined value exceeds €50,000 on December 31 of the relevant year, all of them must be declared. Category two covers foreign securities, investment funds, life insurance policies, and pension-equivalent products (including US 401(k)s and IRAs, UK SIPPs). Category three covers foreign real estate. Each category is assessed independently. Exceeding the threshold in one category does not automatically require declaring the others unless they also individually exceed €50,000. A qualified Spanish tax advisor should review all three categories before your first potential filing year.

References

- Spanish Tax Agency (Agencia Tributaria) — Special Expatriate Tax Regime (Beckham Law, Article 93 LIRPF) (opens in new tab)

- OECD — Common Reporting Standard: Participating Jurisdictions and Technical Documentation (opens in new tab)

- Spanish Ministry of Foreign Affairs — Digital Nomad Visa Official Requirements (2026) (opens in new tab)

- Baleario — Modelo 720 Foreign Assets Declaration: Thresholds, Categories, and Filing Rules (2026) (opens in new tab)

- JURO Spain — Digital Nomad Visa Tax and Social Security: Beckham Law vs RETA (2026) (opens in new tab)