You have a high-net-worth portfolio and want to buy real estate or acquire new business assets. However, you absolutely do not want to sell your current holdings and trigger massive capital gains taxes. Lombard loans for offshore bank accounts provide the exact financial solution you need. This advanced wealth management strategy allows you to borrow cash against your existing international investments. Therefore, you gain immediate purchasing power while your original portfolio remains fully intact and continues to generate returns. Let’s break down how this powerful tool uses tax neutrality and leverage to safely scale your global assets.

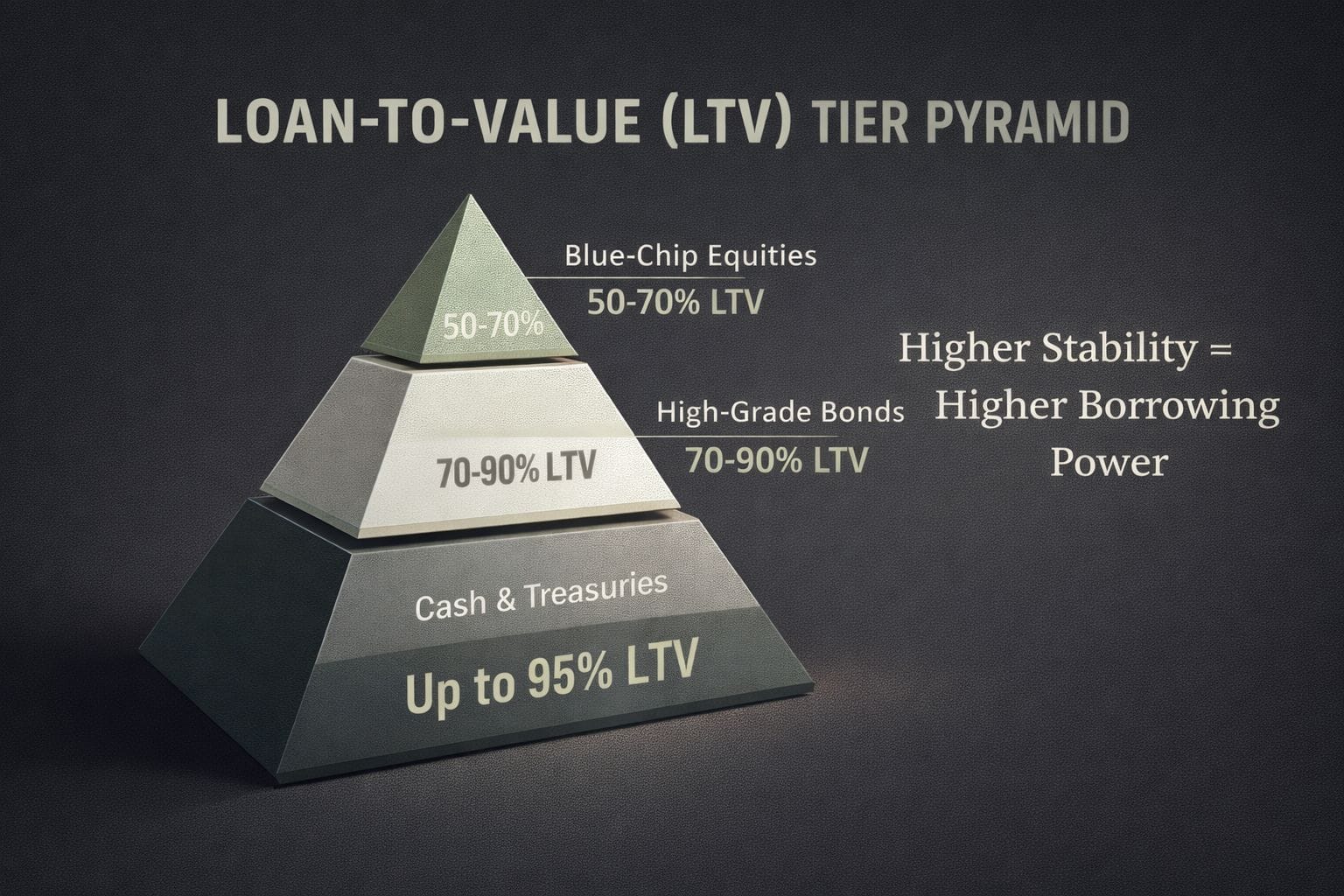

Visualizing Your Borrowing Power

Different asset classes provide varying levels of liquidity. This chart illustrates how safer, lower-volatility assets yield significantly higher borrowing power (Loan-to-Value) compared to speculative assets.

What is a Lombard Loan in Offshore Banking?

A Lombard loan is a specialized credit facility secured by your liquid assets. Instead of proving your income to secure a traditional mortgage, you pledge your investment portfolio as collateral. Banks grant you a revolving credit line based on the quality and volatility of those pledged assets.

Here is why this matters:

When you utilize Lombard loans for offshore bank accounts, you bridge the gap between global wealth and local purchasing power. Your assets stay safely domiciled in a secure jurisdiction, such as Switzerland or Singapore. Meanwhile, you receive cash in your preferred currency to deploy wherever you need it.

The Core Mechanics of Collateral

Banks do not lend dollar-for-dollar against your investments. Instead, they apply a Loan-to-Value (LTV) ratio. This ratio acts as a protective buffer for the institution. If your assets fluctuate in value, the bank knows its capital remains secure.

Furthermore, you retain complete ownership of your portfolio. You continue to collect all dividends, interest payments, and capital appreciation. You simply cannot sell or transfer the pledged assets without the bank’s permission until you repay the loan.

The Power of Tax Neutrality

Tax neutrality stands as the single biggest advantage of this financial instrument. High-net-worth individuals constantly seek ways to fund their lifestyles without enriching the tax authorities.

Avoiding Capital Gains Tax

Selling assets triggers immediate tax liabilities. If your portfolio has grown significantly, liquidating positions means paying capital gains tax. In many Western countries, this can easily consume up to 30% of your profits.

Lombard loans elegantly solve this problem. Because you never sell the asset, you never trigger a taxable event. The portfolio continues to compound tax-free within your offshore structure.

Why Loan Proceeds Are Not Income

Tax agencies tax income, not debt. When an offshore bank deposits Lombard loan funds into your account, those funds classify as a liability. Consequently, a loan is not taxable income. You can repatriate this capital to your home country to fund a property purchase. You effectively access your wealth with zero immediate income tax or capital gains tax.

However, you must maintain proper documentation. You should always consult a local tax attorney to ensure your corporate structures comply with domestic anti-avoidance regulations.

Decoding Loan-To-Value (LTV) Ratios

Banks assess risk meticulously. They assign different LTV ratios based on how easily they can liquidate an asset during a market crash. Let’s explore the standard limits you can expect from premium offshore banks.

Cash and Cash Equivalents

Cash represents the ultimate safe haven for lenders. If you pledge cash or short-term treasury bills, banks usually offer the highest leverage available.

- Typical LTV: 90% to 95%.

- Best Use Case: Currency hedging. You might hold Swiss Francs but need US Dollars to buy a property in Miami.

High-Grade Bonds

Government bonds and highly rated corporate debt carry low volatility. Banks favor these assets heavily.

- Typical LTV: 60% to 90%.

- Best Use Case: Steady, low-risk portfolio expansion. The bond yield often covers the interest cost of the loan.

Blue-Chip Equities

Stocks experience daily price swings. Therefore, banks apply stricter haircuts to equity portfolios to protect themselves against sudden market downturns.

- Typical LTV: 40% to 70%.

- Best Use Case: Aggressive wealth building. For example, pledging €500,000 in LVMH stock might secure a €375,000 credit line.

Leveraging Your Portfolio for Real Estate

Real estate investors frequently utilize Lombard loans for offshore bank accounts to dominate competitive property markets. Cash buyers always hold the upper hand in real estate negotiations.

The Step-by-Step Purchasing Framework

Let’s break down exactly how you execute this strategy.

- Pledge the Assets: You instruct your offshore private bank to ring-fence a portion of your stock portfolio.

- Secure the Credit Line: The bank approves a Lombard limit within 48 hours.

- Draw Down Funds: You transfer the required cash directly to the escrow agent or property seller.

- Acquire the Property: You close the deal as a cash buyer, securing the property without mortgage contingencies.

- Service the Debt: You pay the monthly interest using your portfolio’s dividend yields.

Ultimately, you now own two appreciating assets. Your stock portfolio continues to grow offshore, and your new real estate property appreciates domestically.

Lombard Loans vs. Traditional Mortgages

Traditional mortgages require endless paperwork. Banks scrutinize your tax returns, business income, and credit score. Furthermore, the underwriting process can take months.

Conversely, Lombard lending focuses entirely on asset quality. If your collateral meets the criteria, the bank approves the loan almost instantly. You bypass the invasive income verification process entirely.

Risk Management: Navigating the Margin Call

Leverage amplifies gains, but it also magnifies losses. You must understand the risks associated with asset-backed lending. The most critical threat to your wealth is the margin call.

What Triggers a Margin Call?

A margin call occurs when the value of your pledged portfolio drops below the bank’s required safety threshold. Financial markets can drop rapidly. If your stock portfolio loses 25% of its value in a week, your LTV ratio spikes dangerously high.

The bank will instantly contact you. They will demand that you either deposit more cash or pledge additional securities.

Defensive Strategies to Protect Your Wealth

Smart investors never borrow up to their maximum limit. If the bank offers a 70% LTV, you should only draw down 40%. This leaves a massive buffer to absorb market shocks.

Additionally, you must diversify your collateral. Do not pledge a single volatile tech stock. Instead, pledge a broadly diversified index fund. Broad markets rarely crash as violently as individual stocks.

If you fail to meet a margin call, the bank holds the legal right to liquidate your assets without your permission. They will sell your stocks at the absolute bottom of the market to recover their loan. This locks in catastrophic losses.

Strategic Currency Alignment

Currency risk represents a hidden danger in offshore borrowing. You might pledge a portfolio denominated in Euros to borrow US Dollars.

If the Euro suddenly collapses against the Dollar, the value of your collateral shrinks in Dollar terms. Consequently, this currency shift alone could trigger a margin call, even if your underlying stocks performed perfectly.

Always try to align your loan currency with your collateral currency. If you must cross currencies, work with your wealth manager to implement proper hedging strategies using forward contracts.

Expert Insights on Offshore Leverage

Financial authorities continuously update international banking regulations. In 2026, transparency remains paramount. The Common Reporting Standard (CRS) ensures that your home country knows about your offshore accounts.

Therefore, secrecy no longer protects offshore wealth. Tax neutrality relies entirely on the legal fact that debt is not income. You must structure these loans purely for economic purposes, not for hiding assets. Regulatory bodies actively look for “abuse of law” structures that lack genuine economic substance.

Use reputable private banks in Switzerland, Liechtenstein, or Singapore. These jurisdictions offer the deepest expertise in structuring complex, cross-border Lombard facilities legally and transparently.

Is an Offshore Lombard Loan Right for You?

Before you sign a credit agreement, weigh the operational pros and cons.

The Strategic Advantages:

- Instant liquidity without selling assets.

- Tax-neutral wealth extraction.

- Ability to act as a cash buyer for real estate.

- Interest rates often sit lower than unsecured personal loans.

The Notable Disadvantages:

- Severe margin call risks during market crashes.

- Complex currency risk management requirements.

- Potential legal scrutiny if structured poorly.

Ultimately, Lombard loans for offshore bank accounts serve as an elegant instrument for sophisticated investors. They unlock the true purchasing power of your wealth.

Frequently Asked Questions

Take the Next Step

Managing global wealth requires precision, strategy, and the right financial partners. Before you can explore advanced leverage strategies like Lombard loans, the fundamental first step is establishing a secure banking relationship in a premium jurisdiction.

If you are ready to build that foundation, Easy Global Banking offers specialized assistance to seamlessly open a Swiss bank account. Their expert team helps high-net-worth individuals navigate international compliance and connect with top-tier banking institutions, giving you the infrastructure needed for sophisticated portfolio management.

Disclaimer

This article is strictly for informational and educational purposes and does not constitute financial, legal, or tax advice. We do not offer, underwrite, broker, or promote credit services, Lombard loans, or any specific financial products. Utilizing leverage and asset-backed lending involves significant risk, including the potential loss of your underlying collateral due to market volatility. Always consult with a certified financial planner, tax attorney, or licensed wealth manager in your jurisdiction before making any borrowing, investment, or offshore banking decisions.