If you get your crypto income documentation bank application wrong in 2026, your bank can freeze or even close your account without warning. As a result, many crypto investors feel more scared of their compliance officer than of market volatility. I see this every week when clients come to me with blocked wires and panicked emails from their banks.

My name is Asel Mamytova. I am the founder of Easy Global Banking and a certified cross-border banking and AML expert. Before that, I worked for years at a FINMA‑regulated Swiss asset management firm, sitting on the same side of the table as the compliance officers who now review your files. I know exactly why they reject crypto funds — and, more importantly, how to present your story so they approve them.

Why Traditional Banks Fear Crypto in 2026

From the bank’s point of view, crypto is not “innovative.” It is high regulatory risk until you prove otherwise.

Global rules now treat virtual assets much like traditional finance. FATF Recommendation 15 extends full AML and KYC obligations to crypto businesses and virtual asset service providers (VASPs), including licensing, monitoring, and suspicious activity reporting. Therefore, when your money touches an exchange or on-chain wallet, your bank must be able to explain that path to its own regulators.

In the EU, MiCA fully took effect on 30 December 2024 and continues to tighten expectations around crypto‑asset service providers through 2025–2026. As a result, banks now see any unexplained crypto inflow as a direct risk of fines, forced account closures, and licence problems.

So they take the simple route:

- If they cannot understand your crypto history, they say no.

- If they can understand and evidence it, they keep the relationship.

My job in this article is to show you how to move from the first group to the second.

The Core Elements of a Crypto Income Documentation Bank Application

Most people think banks “hate crypto.” In reality, they hate messy files. A strong crypto income documentation bank application tells a clean story from start to finish: who you are, how you earned the money, and how it moved.

Think in three layers:

- Who you are — identity, country of tax residence, professional profile

- How you made the money — trading, long‑term investing, mining, staking, business income

- How the funds moved — from fiat into crypto, between wallets and exchanges, and finally back into fiat

When these three layers match, the compliance officer relaxes. When they clash, the officer starts drafting a suspicious activity report.

How to Prove Crypto Gains to Bank Officers

Clients often ask me how to prove crypto gains to bank staff in a way they actually accept. I always answer with the same rule: start with fiat, end with fiat, document everything in between.

Here is the basic paper trail you need:

- Initial fiat deposits into exchanges

- Bank transfer receipts from your existing fiat bank to each exchange

- Screenshots or PDFs showing deposit confirmations

- Exchange trade history

- CSV export of your trading history from regulated exchanges (Binance, Coinbase, Kraken, etc.)

- Clear summary of major profitable trades or long‑term holdings

- On‑chain movement overview (if relevant)

- Explorer links for large transfers between your own wallets

- Simple diagram (even in PowerPoint) showing the flow between wallets

- Final fiat withdrawals

- Withdrawal confirmations from the exchange back to your bank

- Matching credit entries on your bank statements

When you build your crypto income documentation bank application, you want the compliance officer to trace every large movement in three clicks or less. Therefore, avoid throwing 200 random screenshots at them. Instead, group documents by theme and label them clearly.

Mastering Crypto KYC: Wallets, Exchanges, and Chain Analysis

In 2026, crypto KYC is not just for exchanges. It indirectly shapes how your bank judges you as a client.

Regulators now expect crypto‑asset service providers to reach traditional banking‑level standards for KYC, transaction monitoring, and sanctions screening. Consequently, banks feel more comfortable when your history runs through regulated, KYC’d exchanges instead of anonymous peer‑to‑peer trades.

Here is how you align your setup with what banks prefer:

- Use regulated exchanges for major on‑ and off‑ramps.

Platforms that follow FATF and MiCA rules log your KYC data and keep auditable records. - Prove you own your wallets.

Some banks or crypto‑friendly intermediaries now ask for:- A small “Satoshi test” transaction from the wallet to a specified address

- A signed message from the wallet’s private key

- Screenshots from wallet apps showing your name or verified account ID

- Accept that banks use chain analysis tools.

Many institutions work with providers that flag coins touching mixers, sanctioned entities, or dark‑web services. If your coins carry that taint, the bank may block them regardless of your personal story.

Moving forward, always ask yourself: “If a stranger looked at these flows with a blockchain analysis tool, would they see a clean pattern or a mess?” That is exactly what your compliance officer sees.

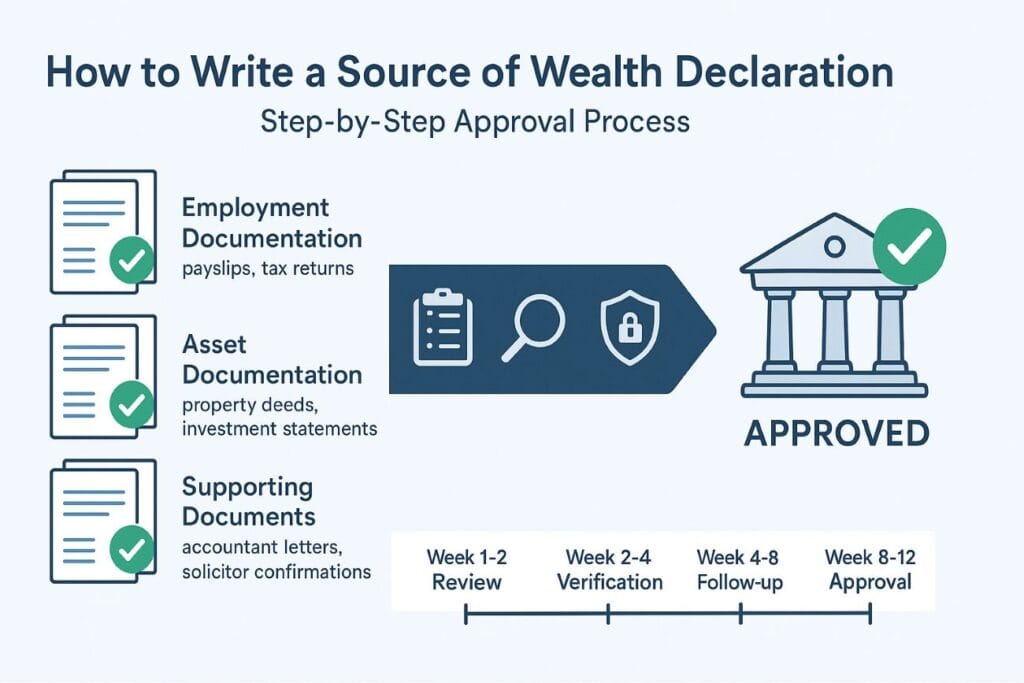

Structuring Your Source of Wealth Crypto Bank Report

Most clients underestimate how much a well‑written source of wealth crypto bank report changes the outcome. Your documents show what happened. The report explains why it makes sense.

You want to give the officer a short, structured story they can copy into their internal file. Here is the compliance package I recommend:

1. Narrative report (2–3 pages, max)

Outline:

- Your professional background and main non‑crypto income sources

- When and why you entered crypto

- Your main strategy (trading, long‑term holding, mining, business)

- The size of your initial investments and how they grew

- Key dates and events (bull runs, major cash‑outs)

2. CPA or tax advisor letters

- Letter confirming you declared your crypto income or gains where required

- Basic numbers: total realised gains, tax paid or payable, and the period covered

- Confirmation that your current wealth level matches your tax filings

3. Transaction history bundle

- Exchange statements showing the path Fiat → Exchange → Crypto → Exchange → Fiat

- On‑chain explorer links for large wallet‑to‑wallet transfers

- Simple table summarising the biggest positions and exits

4. Identity‑linked wallet and account screenshots

- Screenshots from exchanges showing your verified profile and current balances

- Wallet app screenshots tying key addresses to your control

- Any chain analysis reports you obtained voluntarily to show funds are clean

This package turns your crypto income documentation bank application from a random pile of screenshots into a clear, defensible story that a risk committee can accept.

Red Flags That Ruin a Crypto Income Documentation Bank Application

I often see a good crypto income documentation bank application destroyed by three avoidable red flags. Compliance teams react very strongly to each of them.

1. Mixers and privacy tools

- Use of mixers like Tornado Cash, CoinJoin, or similar services

- Heavy reliance on privacy coins with weak documentation

From the bank’s view, these tools hide the origin of funds and create direct FATF risk. Therefore, many institutions have a simple policy: any coins that touched a mixer are off‑limits.

2. Large peer‑to‑peer trades with strangers

- High‑volume P2P activity on unregulated platforms

- OTC trades with no contracts, invoices, or IDs

These flows look like unlicensed money services or informal remittance businesses. As a result, even if you did nothing wrong, the bank sees unmanageable risk.

3. Sudden massive deposits with no history

- A dormant account suddenly receives a six‑figure crypto cash‑out

- No previous pattern of investing or saving at that level

Banks must explain jumps in wealth to regulators. If your file lacks a long‑term build‑up story, they fear tax evasion, insider trading, or other offences — even if your gains were legal.

When one of these red flags appears, officers often decide it is easier to say no and move on to the next case.

Next Steps for Securing Your Fiat Account

Cashing out crypto safely in 2026 is no longer about “finding a friendly bank.” It is about presenting a file that any responsible bank can defend to its supervisor.

If you want a stable fiat setup, here is the path I recommend:

- Start building your documentation months before you plan to cash out

- Use regulated exchanges as your main on‑ and off‑ramps wherever possible

- Keep a clean, labelled archive of statements, CSV exports, and wallet evidence

- Write a clear financial story that links your career, your risk profile, and your crypto gains

- Avoid mixers, shady OTC desks, and “fast track” tricks that create permanent stains on your coins

If your current history is already messy, do not panic. You can still improve the picture with better documentation and a structured explanation — but you should not attempt that alone.

Need help turning your crypto history into a bank‑ready file?

At Easy Global Banking, I work with crypto‑rich clients who want safe, long‑term access to fiat banking in serious jurisdictions like Switzerland, Singapore, Monaco, and Puerto Rico. My team:

- Reviews your current crypto trail from a Swiss AML perspective

- Builds a full documentation package and source of wealth report

- Prepares you for bank questions and connects you with crypto‑tolerant institutions where appropriate

If you want your next large cash‑out to feel boring instead of terrifying, we can help you get there.

📩 Contact Easy Global Banking for a Private Crypto Compliance Review