The answer is almost never what the bank tells you. After years of guiding high-net-worth clients through Swiss private banking, I have seen every version of this rejection — and I can tell you that most of them were entirely preventable.

Every year, thousands of non-residents, entrepreneurs, and family offices apply to open a Swiss bank account as a non-resident. Most of them receive a rejection they never fully understand. I know this because many of them eventually find their way to my desk.

The letter, when it arrives at all, is a masterpiece of legal non-commitment. “We are unable to proceed with your application at this time.” No reason. No guidance. No second chance. Just silence, wrapped in polite Swiss formality.

What I want to share in this article is what that letter does not tell you — the real reasons Swiss bank account applications get rejected, drawn from years of working directly inside this process. I will also show you what to do about it, because in my experience, the vast majority of rejections are fixable.

First, a few numbers to set the scene:

- Switzerland manages over CHF 9.2 trillion in banking assets across 230 institutions, yet fewer than 30% of those institutions actively onboard non-resident clients.

- Swiss banks manage approximately 25% of all global cross-border private assets — more than any other country.

- Nearly 50% of Swiss banking clients are based abroad, yet non-resident rejection rates remain disproportionately high due to compliance costs.

In other words: the market is enormous, the appetite exists, but the bar for entry is genuinely high — and deliberately so. Let me explain why, and more importantly, let me explain what actually determines which side of that bar you land on.

The Most Common Rejection Reasons — At a Glance

Before I walk through each reason in depth, here is a summary of what I see most often in my work with clients whose Swiss bank account applications have been rejected:

| Rejection Reason | Frequency in My Experience | Fixable? |

| Wrong bank selected for client profile | Very Common | ✓ Yes — bank matching |

| Weak or incomplete Source of Wealth | Most Common | ✓ Yes — documentation rebuild |

| Opaque corporate structure / unclear UBO | Common | ✓ Yes — structure narrative |

| High-risk nationality or country of residence | Common | Partially — bank selection key |

| Cold application without warm introduction | Very Common | ✓ Yes — relationship access |

| Prior rejection on record, unresolved | Frequent | ✓ Yes — root cause analysis |

| Politically Exposed Person (PEP) status | Less Common | Partially — specialist banks |

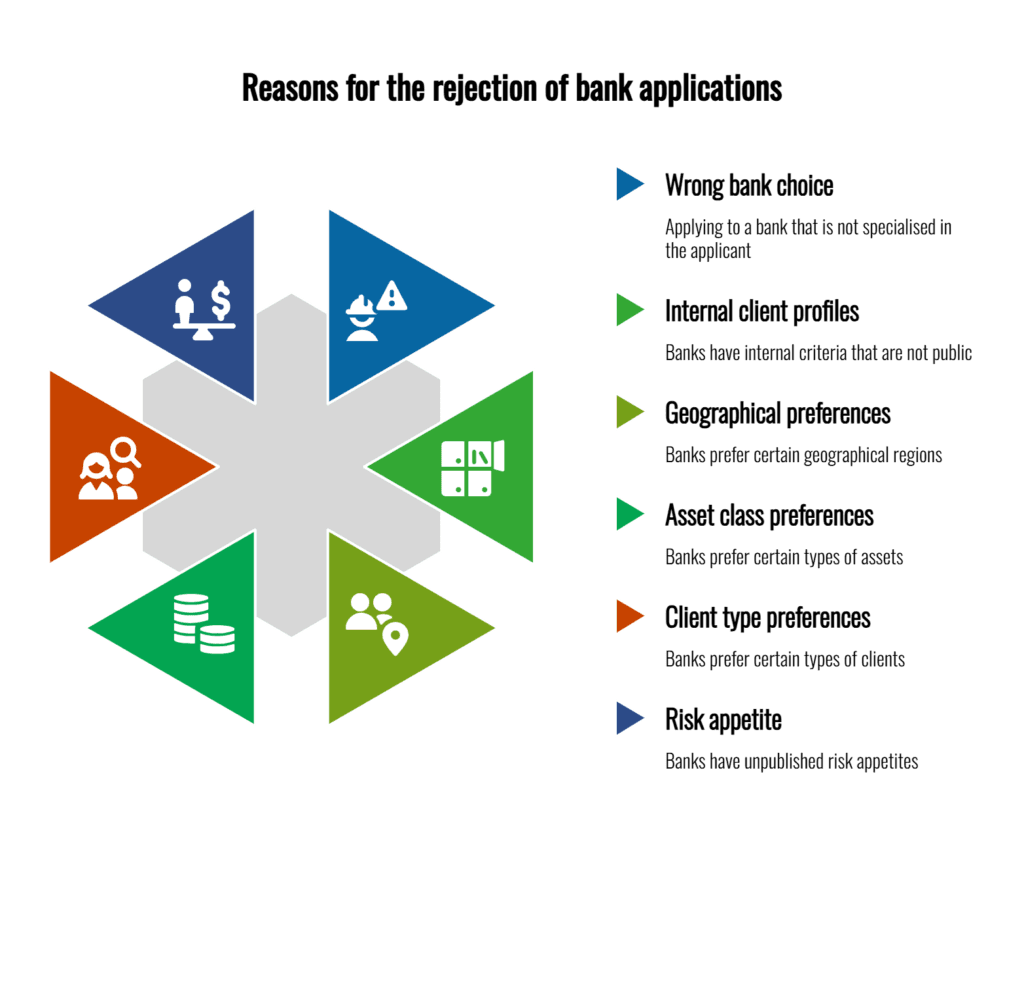

1. You Applied to the Wrong Bank Entirely

This is, without question, the most quietly devastating mistake — and it is the one I encounter most often. Switzerland has over 200 licensed banking institutions. They are not interchangeable.

Each bank maintains an internal client profile: a preferred geography, a preferred asset class, a preferred client type, and — critically — an unpublished risk appetite that determines which nationalities, industries, and corporate structures they will even consider. None of this appears on their website.

Consequently, a bank that specialises in serving European family offices will evaluate a non-resident holding company from Southeast Asia very differently from a bank with established relationships in that region. The application looks identical. The outcome is completely different.

What I see clients get wrong, time and again:

- Applying to a well-known Swiss institution simply because they have heard of it — without checking whether that bank actively onboards clients from their country of residence.

- Assuming that a rejection from one bank means Swiss banking is not available to them at all.

- Not knowing that certain banks maintain informal internal flags by nationality, industry sector, or holding structure type — none of which are disclosed publicly.

💡 Insider Tip: Before submitting any application, research which Swiss banks have actively opened accounts for clients with your exact profile — your country of residence, your industry, and your corporate structure type. This knowledge lives inside professional networks, not on any public database. It is the first thing I check for every client I work with.

2. Your Source of Wealth Story Did Not Hold Up

I want to be direct about this one, because it is the rejection reason that surprises people the most. Your source of wealth declaration is not a formality. It is the spine of your entire application.

Swiss compliance officers are trained to read a Source of Wealth (SOW) statement the way a detective reads a witness statement — looking for gaps, inconsistencies, and things that do not quite add up. Moreover, they cross-reference your declaration against your public footprint, your company records, and any available financial filings.

The most common SOW failures I encounter look like this:

- “Profits from my business” — submitted without company accounts, audited financials, or tax returns to support the figure.

- Real estate proceeds that cannot be traced to a verifiable sale transaction with documentation.

- Inheritance wealth without estate documentation, probate evidence, or a legal letter from the executor.

- Cryptocurrency gains stated without exchange records, wallet histories, or conversion documentation.

A client came to me after being rejected by two separate Swiss private banks. His wealth originated from the sale of a software company — entirely legitimate, well-documented if you knew where to look. The problem? His SOW declaration said only “sale of business interests.” When I rebuilt his application with the full acquisition agreement, the acquiring company’s details, the escrow confirmation, and the wire transfer trail to his personal account — the picture was complete. He had not failed the compliance test. He had simply failed to present the answer clearly enough for a compliance officer with twenty minutes and a checklist.

💡 Insider Tip: Think of your SOW not as a form to fill in, but as a story to prove. Every significant wealth event — a business sale, an inheritance, an investment exit — needs a beginning, a middle, and a paper trail at the end.

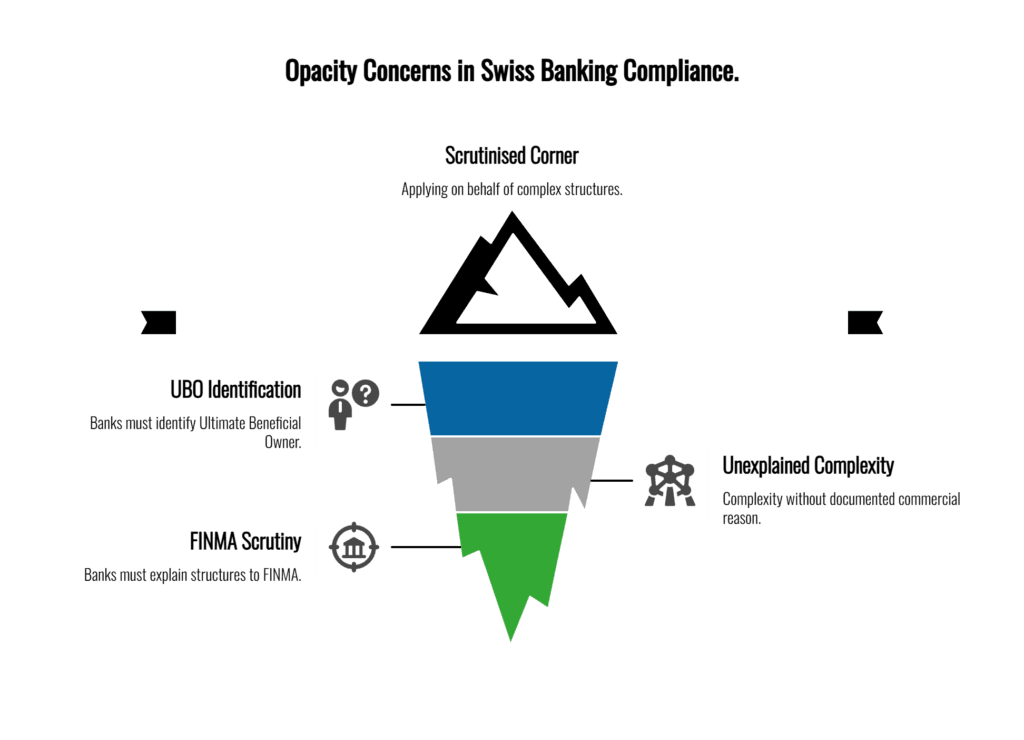

3. Your Corporate Structure Triggered Opacity Concerns

If you are applying on behalf of a holding company, a trust, or a multi-jurisdictional structure, you are entering the most scrutinised corner of Swiss banking compliance — and rightly so.

Swiss banks have a legal obligation under FINMA regulations to identify the Ultimate Beneficial Owner (UBO) of every account. This sounds straightforward — until your structure involves a BVI holding company owned by a Cayman foundation with a discretionary trust layer and nominee directors. At that point, what the compliance team sees is not sophistication. It is complexity they cannot easily document for a regulator.

Complexity is not the problem. Unexplained complexity is.

Every layer of your corporate structure needs a documented commercial reason for existing. Tax efficiency is acceptable. Asset protection is acceptable. Legitimate estate planning is acceptable. What is not acceptable — or rather, what banks simply will not take the risk of accepting — is a structure they cannot clearly explain in writing if FINMA ever asks.

💡 Insider Tip: Prepare a one-page structure chart with a written narrative: why each entity exists, where it is registered, who controls it, and what its commercial purpose is. Present this proactively as part of your application package. Banks respond very differently when they receive clarity they did not have to ask for.

4. Your Nationality or Residency Triggered Automatic Screening

This is the rejection nobody talks about openly, because it feels discriminatory. It is not — it is a regulatory and risk management reality. But understanding it clearly can save you months of wasted effort.

Swiss banks maintain internal country risk lists that are entirely separate from, and often stricter than, the official FATF grey and black lists. These are not published anywhere. They reflect each institution’s own regulatory exposure, historical compliance incidents, and what their compliance team is prepared to defend in front of FINMA.

Additionally, two specific regulatory frameworks create automatic barriers for certain applicants:

- US citizens and Green Card holders face FATCA reporting obligations that lead many Swiss banks — particularly smaller private institutions — to decline applications outright rather than absorb the compliance cost.

- Following the Swiss Federal Council ordinance of June 2022, Swiss banks are required to reject nearly all applications from Russian and Belarusian nationals, with only narrow exceptions for those with verified EU or UK legal residency and demonstrably clean, non-sanctioned funds.

If your nationality or country of residence appears on a bank’s internal high-risk list, your application may be declined automatically — before a human relationship manager ever reads a single page of your documentation.

The solution is not to conceal your background. It is to identify the specific banks that actively welcome clients from your country today — and to approach only those institutions.

5. You Submitted a Cold Application Without a Warm Introduction

Swiss private banking has operated on relationships for over three centuries. That is not a romantic notion — it is a commercial reality that directly affects application outcomes.

When you submit a cold application through a bank’s website, or through a lawyer or accountant who has no personal standing with that institution, you start with a trust deficit that the application itself rarely overcomes. The compliance team has no relationship context. They see a file, not a person.

By contrast, when a known intermediary or an existing client introduces you to a relationship manager directly, the dynamic shifts entirely. The bank’s default posture changes from “why should we accept this?” to “how do we make this work?” The file is the same. The starting position is completely different.

Over the years, I have seen technically flawless applications rejected from cold submissions, and applications with complex profiles approved through warm introductions — simply because someone in the bank was willing to champion the relationship internally. Access to those introductions is not luck. It is the core of what a good banking consultant actually provides.

6. A Previous Rejection Followed You to the Next Bank

This is the rejection dynamic that creates more rejections, and it is almost entirely unknown to applicants until it is too late.

When you apply to a Swiss bank and get declined, you will very likely be asked on your next application whether you have previously applied to a Swiss bank and been turned down. This is standard KYC practice. Answering dishonestly carries serious legal consequences. Answering honestly — without a credible explanation for what has changed — raises an immediate red flag.

Furthermore, the Swiss private banking world is smaller than it appears. Compliance professionals move between institutions. Relationship managers maintain industry networks. A rejection at one institution does not always stay quietly within that institution’s walls.

💡 Insider Tip: If you have been rejected, resolve the root cause before applying anywhere else. Submitting a new application to a different bank — without understanding and addressing what triggered the first rejection — simply accelerates a second one. And the cumulative pattern of multiple declines becomes progressively harder to overcome the longer it continues.

Understanding the Swiss Bank Application Process — And Where It Breaks Down

To understand where rejections occur, it helps to understand how Swiss banks actually process applications. Here is what typically happens behind the scenes — and where I most commonly see things go wrong:

| Phase | What the Bank Is Doing | Common Failure Point |

| Week 1–2 | Initial profile screening — does your nationality, asset level, and structure fit their appetite? | Wrong bank: automatic no before anyone reads your file |

| Week 3–4 | Relationship manager review — KYC checks, Google screening, sanctions lists | Unexplained press coverage, public records, or listed directorships |

| Week 5–8 | Compliance documentation review — SOW, UBO, corporate structure | Missing documents, inconsistent figures, untraceable wealth trail |

| Week 9–12 | Enhanced Due Diligence (EDD) — deeper verification if any flags raised | Prior rejections disclosed without explanation of what changed |

| Week 13+ | Final decision | Cumulative doubt from multiple small red flags |

The Question Nobody Asks: What Does the Bank Actually See?

When clients come to me after a rejection, the first thing I do is not prepare a new application. I conduct what I call a compliance audit — an objective assessment of how this client appears to a bank, on paper, in twenty minutes.

I look at their digital footprint. I examine how their corporate structures are described in public registries. I review any press coverage, litigation history, or regulatory mentions that would surface in a standard KYC database search. I read their Source of Wealth declaration as if I am a compliance officer who has never met them.

What I find, consistently, is this: most rejected applications were not rejected because of who the client is. They were rejected because of how the client appears to someone with limited time, a compliance checklist, and no prior relationship.

That is the gap that proper preparation and experienced guidance closes.

So, What Should You Do If Your Swiss Bank Account Application Was Rejected?

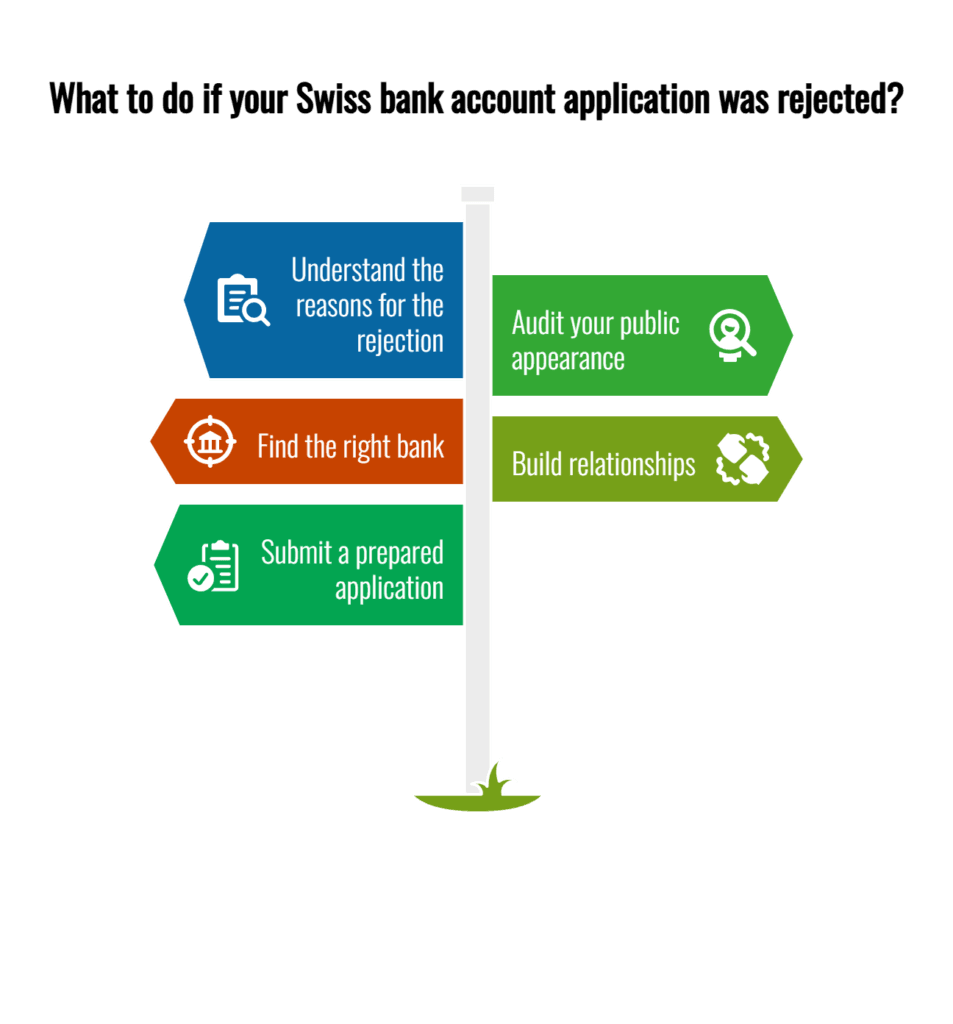

First, do not immediately apply to another bank. That instinct is understandable, but it often compounds the problem rather than solving it.

Instead, take these steps:

Then, and only then, submit a fully prepared, strategically positioned application.

- Understand precisely why the rejection occurred — not the polite form letter, but the underlying compliance trigger.

- Audit how you appear from the outside: your public records, your corporate structure documentation, your Source of Wealth presentation.

- Identify the right Swiss institution for your specific profile — one that actively onboards clients from your country, in your industry, with your type of structure.

- Build or access the relationship introduction that changes your starting position from cold applicant to referred client.

Swiss private banking is not closed to non-residents. It is not closed to entrepreneurs, family offices, or complex holding structures. It is, however, a process that rewards preparation — and punishes assumptions.

At BMA Business Solutions, I work only with clients I am confident I can get approved. That confidence is why I back every engagement with a 100% money-back guarantee. I have spent years building the relationships, the knowledge, and the preparation process that transforms rejected applicants into approved account holders — typically within weeks, not months.

Ready to Open Your Swiss Bank Account — Without the Rejection Risk?

Book a free consultation with me directly. I review your profile personally, identify the right institution, and guide you through every step of the process.

Minimum investable assets: CHF 500,000 | 100% money-back guarantee